Mid-June brought heightened geopolitical tension as Israel launched a surprise strike on Iran’s nuclear facilities, triggering fears of a broader regional conflict. Oil surged over 10% in a matter of days, stoking inflation concerns and weighing on equity markets. Risk-sensitive sectors such as airlines, shipping, and industrials faced sharp drawdowns as investors recalibrated expectations for growth and profitability.

Yet, by June 23, tensions unexpectedly eased. A ceasefire agreement between Israel and Iran triggered a reversal in oil prices, which dropped nearly 7%, and a rapid rebound in global equities. The sudden turnaround underscored the market’s capacity for resilience and its ability to price in risk efficiently. It also served as a reminder that short-term volatility, often driven by geopolitical events, can offer opportunities for disciplined investors when accompanied by longer-term structural tailwinds.

In this case, sectors most impacted during the selloff, including transportation, materials, and cyclicals, bounced back sharply once tensions cooled. Investors rotated back into risk assets with confidence, encouraged by the swift return of stability in commodity markets and the absence of broader military escalation.

Tariffs Take Center Stage

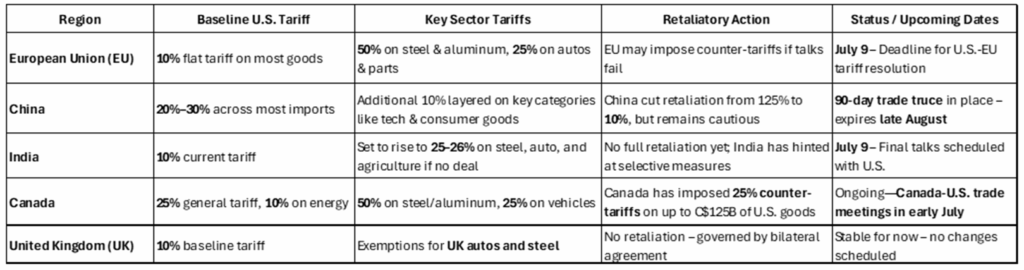

With Middle East concerns subsiding, global attention has shifted to tariffs and trade negotiations. The U.S. is simultaneously renegotiating key trade relationships with Canada, the EU, India, and China. Though no major economic impacts have materialized yet, investors remain cautious. Tariffs on goods have historically slowed growth and raised prices, but the current market environment has proven surprisingly resilient supported by strong earnings in technology, stable consumer demand, and expectations of central bank easing.

July will be a critical month as several deadlines approach. The U.S. and EU are nearing the end of a grace period to resolve disputes over digital services taxation and industrial subsidies. Meanwhile, India’s temporary tariff suspension expires mid-month, and U.S.-China negotiators must revisit the terms of a fragile 90-day trade truce before the end of August. Each of these scenarios carries implications for global supply chains, input costs, and inflation.

Market participants are keeping a close watch on outcomes. While headlines may drive short-term volatility, companies continue to adapt by diversifying supply chains, investing in automation, and passing limited cost increases to consumers. Investors, in turn, are positioning portfolios to favor domestic producers, pricing power leaders, and sectors less exposed to global trade friction.

Canada-U.S. Trade Relations: A Fragile Truce

Tensions between Canada and the U.S. escalated in late June after Ottawa implemented a 3% Digital Services Tax (DST) on U.S. tech giants, retroactive to 2022. President Trump condemned the move, halted all trade talks, and threatened steep new tariffs. Canada responded with a 50% retaliatory tariff on excess U.S. steel imports. Just days later, in a strategic reversal, Canada announced it would suspend the DST, leading to a resumption of talks aimed at finalizing a trade agreement by July 21. The immediate goal is to avoid a snapback of U.S. tariffs currently paused until July 9. (Source: Reuters)

Canada remains one of the most exposed U.S. trading partners, with tariffs of 25% to 50% across major export categories. The economic effects are beginning to show: consumer sentiment is weakening, real estate markets are softening, and businesses in manufacturing and infrastructure are delaying investments. The Bank of Canada has warned that without a resolution, the cumulative impact could tip the economy into recession. A successful resolution in July could significantly improve Canada’s growth outlook.

Domestic Policy Response: Bill C-5

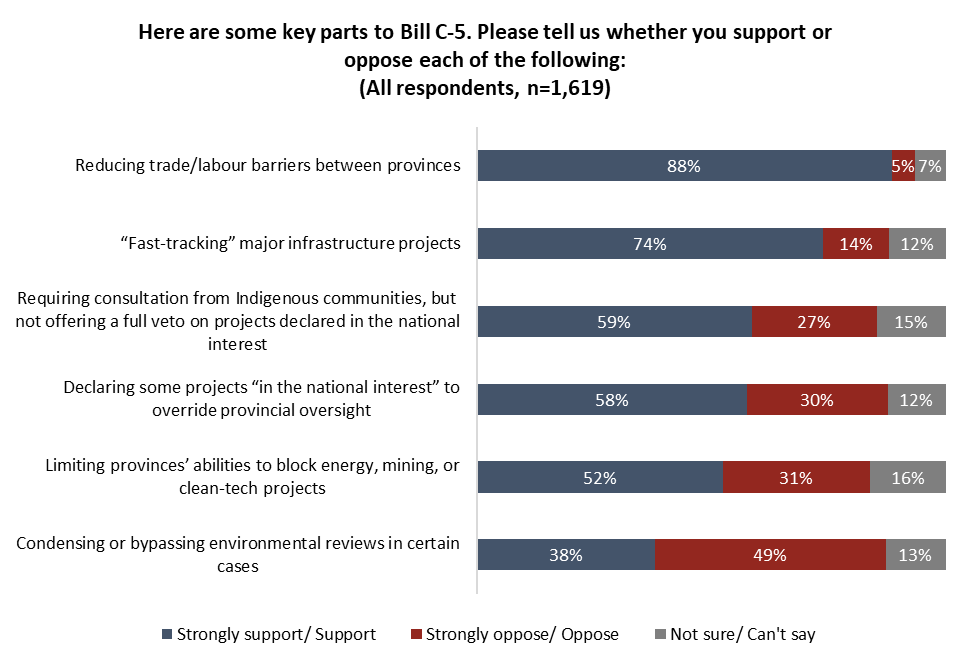

With Bill C‑5 now officially law and receiving Royal Assent on June 26th, Canada has positioned itself to strengthen internal trade, enhance labour mobility, and fast-track critical national infrastructure projects. The government’s next step of engaging in meaningful consultation with provinces, territories, and Indigenous partners marks a thoughtful approach to implementation. If conducted proactively, this process could set new standards for collaborative policymaking and pave the way for strategically important projects to proceed more smoothly and efficiently.

Despite vocal criticism, the bill’s advancement underlines Ottawa’s commitment to economic resilience and nation-building during a time of global uncertainty. As stakeholders collaborate through this summer’s consultation period, there is a real opportunity to balance economic ambition with social and environmental safeguards. If dialogue remains constructive and inclusive, Bill C‑5 has the potential to unite regional or jurisdictional divides, boost productivity, and drive investment, laying the foundation for a more connected and competitive Canadian economy. (Source: CBC)

U.S. Federal Reserve: Policy Signals and Leadership Uncertainty

Markets were also focused on the U.S. Federal Reserve in June, where speculation grew around both interest rate policy and leadership. With inflation cooling and economic momentum slowing, many investors now anticipate a rate cut as early as July or September. Fed Vice Chair Michelle Bowman’s dovish comments reinforced those expectations. Meanwhile, political chatter has surfaced around potential replacements for Chair Jerome Powell, including Kevin Warsh and Kevin Hassett, both seen as more inclined to ease monetary policy. (Source: AP)

The potential for a more accommodative Fed has helped fuel a broad-based rally, particularly in growth sectors and rate-sensitive areas such as housing and consumer discretionary. Bond yields have declined modestly on the back of these expectations, and credit spreads have tightened, reflecting improved investor sentiment. While uncertainty around leadership could complicate forward guidance in the short term, the underlying market narrative remains constructive.

Energy Prices and the Inflation Outlook

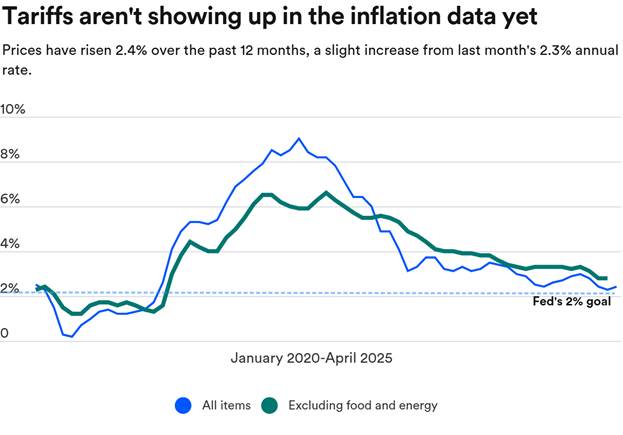

The pullback in oil prices from over $77 to around $65 per barrel has offered a welcome reprieve for inflation-watchers. With energy being a significant driver of costs across the economy, lower oil prices support the broader disinflation trend seen in recent CPI and PCE data. This strengthens the case for a potential rate cut later this year, particularly if economic softening continues. (Source: Trading Economics)

Lower interest rates could help offset some of the price pressures introduced by tariffs, especially on goods imported from Europe and Asia. By easing borrowing costs and supporting consumer spending, central banks can play a crucial role in keeping the recovery on track, even in the face of policy-induced inflation. Additionally, stable or declining oil prices help anchor inflation expectations, a key metric closely watched by policymakers.

Trump’s “One Big Beautiful Bill”

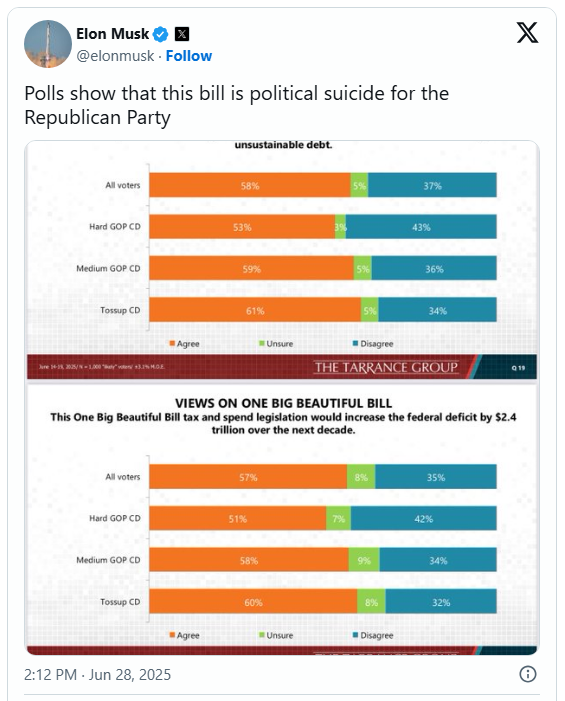

On the fiscal front, President Trump’s sweeping “One Big Beautiful Bill” successfully passed the House in May but has since stalled in the Senate. The $3 trillion proposal combines extensions of the 2017 tax cuts with new immigration initiatives and major healthcare reforms. However, several Medicaid-related cost-saving measures were disqualified under Senate reconciliation rules, prompting Republicans to revise key sections of the bill. Deep divisions within the GOP, between fiscal conservatives and moderates, have further slowed progress. (Source: Washington Post)

Adding to the pressure, prominent voices like Elon Musk have openly criticized the bill, using his platform, X, to denounce its scope and fiscal implications almost daily. If consensus cannot be reached soon, the bill risks becoming entangled in the fall’s looming debt-ceiling negotiations, raising broader concerns around fiscal discipline and the potential impact on Treasury markets.

If passed, the bill could inject further stimulus into the economy, particularly through tax relief and infrastructure funding. Passage would likely boost business sentiment, particularly among small and medium-sized enterprises, and could provide a tailwind to domestic-focused sectors.

Summary:

June presented a whirlwind of headlines from Middle East tensions and trade negotiations to Fed policy shifts and fiscal debates. And yet, despite this backdrop of uncertainty, markets have demonstrated notable resilience. Strong corporate earnings, particularly in tech, continued disinflation trends, and the growing likelihood of central bank support have provided a stabilizing foundation.

Looking ahead, the key to sustained market strength will be policy clarity. If trade negotiations resolve constructively and interest rates ease in line with expectations, the second half of 2025 could mark a period of renewed momentum. For investors, maintaining flexibility and a focus on quality assets will remain essential, but the underlying tone for now is one of cautious optimism. As geopolitical risks ebb and macro conditions stabilize, the stage may be set for a more constructive and broad-based recovery in the months to come.

We thank you for your continued trust and we welcome you to reach out to us with any questions you may have.

This information has been prepared by Kian Ghanei and Terry Fay who are Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.