Over the past two weeks, markets have continued their upward trend, buoyed by a resurgence in investor confidence. Strong corporate earnings, particularly from the technology sector, combined with growing enthusiasm around artificial intelligence and gradually improving macroeconomic indicators have injected optimism into market sentiment. Volatility has declined, and outlooks for the remainder of the year have shifted into a more constructive tone, reinforcing the view that the worst may be in the rearview mirror.

Adding to the positive narrative are signs of stabilization in inflation and softening policy risks. Corporate earnings have surprised to the upside, and recent data suggests inflationary pressures are easing, creating a healthier backdrop for equities. In Canada, markets have quietly gained traction as well, thanks to firm consumer spending, a stable labour market, and early signs of economic resilience. Although threats remain, such as potential 35% tariffs from the U.S. on Canadian exports like steel, autos, and minerals—the domestic market has largely held steady in the face of external uncertainties.

Big Tech and AI-Led Recovery

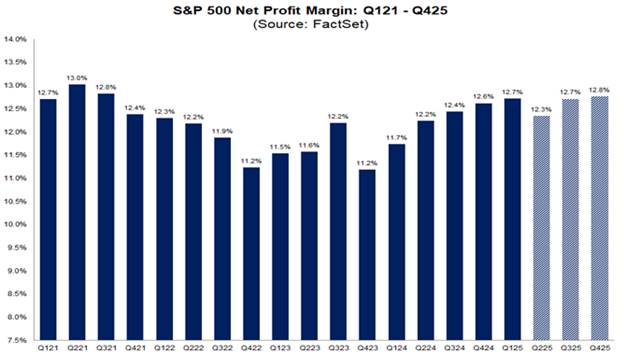

Mega-cap U.S. tech companies such as Alphabet, Nvidia, Microsoft, Amazon, Apple, and Meta have delivered impressive performance in recent weeks, fueled by strong earnings reports and expanded AI investment plans. This wave of momentum reflects broader investor confidence in the transformative potential of artificial intelligence, which continues to drive expectations of long-term revenue growth and margin expansion across the tech sector and beyond. Overall, The S&P 500 is forecasted to continue with the earnings expansion across the breadth of its companies well into Q4 of this year.

Similarly, Morgan Stanley’s projection of a 12% market rally by mid-2026 is underpinned by a combination of strengthening earnings, increased adoption of AI, and policy-driven incentives such as tax breaks embedded in the “One Big Beautiful Bill.” These elements are expected to fuel corporate reinvestment into infrastructure, supply chains, and productivity-enhancing technologies, helping to propel broader economic growth.

AI remains the centerpiece of this renewed optimism. The rapid acceleration in enterprise AI deployment is transforming sectors such as healthcare, financial services, and manufacturing. Even traditional companies that had lagged in digital transformation are now aggressively investing in AI solutions, encouraged by falling implementation costs and rising competitive pressure. The combination of favorable policy incentives and technological advancement is fostering a virtuous cycle of capital expenditure and innovation.

Trade Deal Updates – Progress with Caveats

On the international trade front, the U.S. has made notable progress with key allies over the past month. In a significant development, Washington and Seoul agreed to reduce proposed tariffs from 25% to 15%, paired with South Korea’s commitment to invest $350 billion in the U.S. economy across sectors such as energy and shipbuilding. This was followed by a similar deal with Japan, which agreed to the same 15% tariff level while pledging $550 billion in U.S. investment and greater cooperation in automotive, semiconductor, and agricultural sectors.

Further strengthening global trade momentum, the U.S. reached a framework agreement with the European Union. While most EU exports to the U.S. will be subject to a 15% tariff—down from 30%—some sectors, including steel and pharmaceuticals, will remain in negotiation for possible exemptions. In return, American exports to Europe will regain duty-free access, particularly for critical goods like chemicals and aircraft. In addition, the EU has committed to $600 billion in direct U.S. investments and $750 billion in purchases of American energy and defense equipment.

In contrast, the U.S.–China negotiations have taken a slower, more cautious route. Both sides agreed to a 90-day truce on additional tariffs while discussions continue. For now, U.S. tariffs on Chinese goods stand at 30%, while China maintains 10% tariffs on U.S. products. Although no long-term pact has been finalized, both sides have indicated a willingness to keep the dialogue open, with speculation mounting around a potential Trump–Xi summit later this year.

Canada Under Pressure

Unlike the successful negotiations with Asia and Europe, U.S.–Canada trade talks remain tense and unresolved. With an August 1 deadline, the U.S. has threatened to implement a sweeping 35% tariff on Canadian exports not covered under the USMCA. The delay in securing a deal has been exacerbated by recent political developments, including Canada’s diplomatic stance on foreign policy issues, which has strained cross-border relations.

The consequences of failed talks could be severe. Canada and the U.S. are tightly integrated trading partners, particularly in energy, agriculture, and manufacturing. Over 75% of Canadian exports are U.S.-bound, meaning the potential fallout from a tariff shock could ripple through key sectors. Businesses on both sides of the border are growing increasingly anxious about supply chain disruptions, rising input costs, and the prospect of retaliatory trade measures.

Canada is not alone in facing trade tension. India also remains without a resolution, and a new round of 25% tariffs on Indian exports to the U.S. is set to take effect August 1. Though some Southeast Asian nations have secured temporary relief, unresolved negotiations could complicate global trade flows further if agreements aren’t finalized in the coming weeks.

Canada’s Quiet Strength

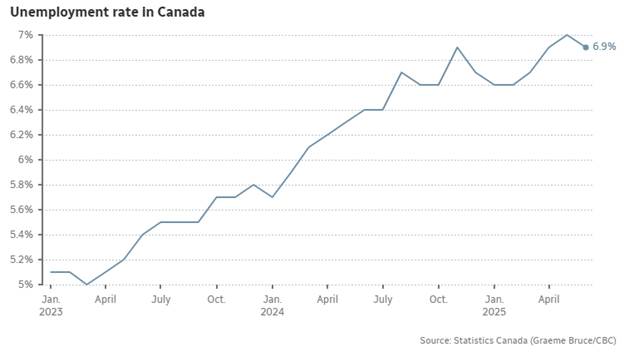

Despite external headwinds, Canada’s economy has shown quiet strength. The June labour market report was particularly encouraging, with 83,100 jobs added—marking the first month of positive employment growth since January. Gains were concentrated in the public sector and service-based industries, and the unemployment rate edged down to 6.9%, indicating underlying stability.

The passage of the One Canadian Economy Act (Bill C-5) represents a step forward in enhancing productivity. The bill aims to eliminate interprovincial trade barriers and expedite national infrastructure projects—long-standing obstacles to economic efficiency. Business leaders have praised the measure, viewing it as a catalyst for increased private investment and intra-provincial trade.

Amid global trade uncertainty, Canada’s internal resilience offers some protection. With steady consumer spending, ongoing hiring activity, and policy progress, the domestic economy appears well-positioned heading into the second half of 2025. While exports and business investment remain vulnerable to geopolitical shifts, internal fundamentals provide a solid anchor.

Central Banks and Rate Outlook

At its July meeting, the U.S. Federal Reserve opted to keep interest rates unchanged at 4.25% to 4.50%. Despite political pressure for cuts, persistently elevated core inflation has led the Fed to maintain its “higher-for-longer” stance. Fed Chair Jerome Powell emphasized a data-dependent approach, noting that premature rate reductions could undermine progress in reining in inflation.

In parallel, the Bank of Canada held its benchmark rate steady at 2.75%, pointing to stabilizing inflation and ongoing trade uncertainty as reasons for caution. While GDP data showed modest contractions in April and May, preliminary figures for June suggest a 0.1% rebound, led by growth in manufacturing, retail, and wholesale trade. The Bank has signaled it will continue to evaluate data closely before making further policy adjustments.

The U.S. Economic Underbelly

Although the U.S. reported 3% annualized GDP growth in Q2, the underlying details are less rosy. Much of the headline strength came from a sharp drop in imports, which artificially inflated growth numbers. When stripping out trade and inventory distortions, real domestic demand grew by just over 1%, pointing to softer momentum beneath the surface.

The labour market, while still strong on the surface, is showing signs of stress. Consumer confidence declined in June, particularly concerning job availability and income prospects. Slower hiring trends and stagnant wages are beginning to impact consumer behavior, especially among mid- and lower-income households who drive much of the nation’s discretionary spending.

Should investor sentiment shift abruptly, due to deteriorating consumer data, an escalation in tariffs, or sticky inflation, this complacency could quickly turn into financial strain, with ripple effects across asset classes.

In Summary

Markets have rallied in recent weeks, led by robust earnings and AI-fueled optimism. The tech sector continues to outperform, while broader economic signals from inflation to jobs have improved. Canada’s economy, though under pressure from external trade risks, has shown resilience with improving GDP projections and supportive policy moves. Meanwhile, global trade deals with major partners have helped temper geopolitical risk, even as unresolved tensions with Canada and India linger.

Nonetheless, caution is warranted. The unresolved U.S.-Canada tariff standoff could trigger economic and political fallout. In the U.S., signs of weakness beneath the surface, sluggish core demand, fragile labour markets, and complacent credit spreads, suggest that the economy may be more vulnerable than headline numbers imply. As the second half of the year unfolds, investors have reason for optimism, but would do well to remain vigilant amid a still-evolving global and economic backdrop.

We thank you for your continued trust and we welcome you to reach out to us with any questions you may have.

This information has been prepared by Kian Ghanei and Terry Fay who are Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.