North American Markets: Balancing Risks and Opportunities into Fall 2025

As we move into the final quarter of 2025, North American markets are being shaped by both challenges and opportunities. Inflation remains higher than central banks would like, trade tensions are weighing on select industries, and housing stress in Canada is creating pockets of vulnerability. These risks have kept volatility elevated and remind investors that caution is still warranted.

At the same time, there are solid reasons for optimism. Corporate earnings have held up, consumers in the U.S. remain broadly resilient, and Canada’s resource sector continues to benefit from strong global demand. Add to that the early signs of monetary easing and major investment in energy transition projects, and the stage is set for markets to keep finding support. For investors, the task now is balancing short-term risks with long-term growth themes that are becoming harder to ignore.

The U.S. Picture: Inflation, Policy, and Tariffs

Inflation Data Driving Policy

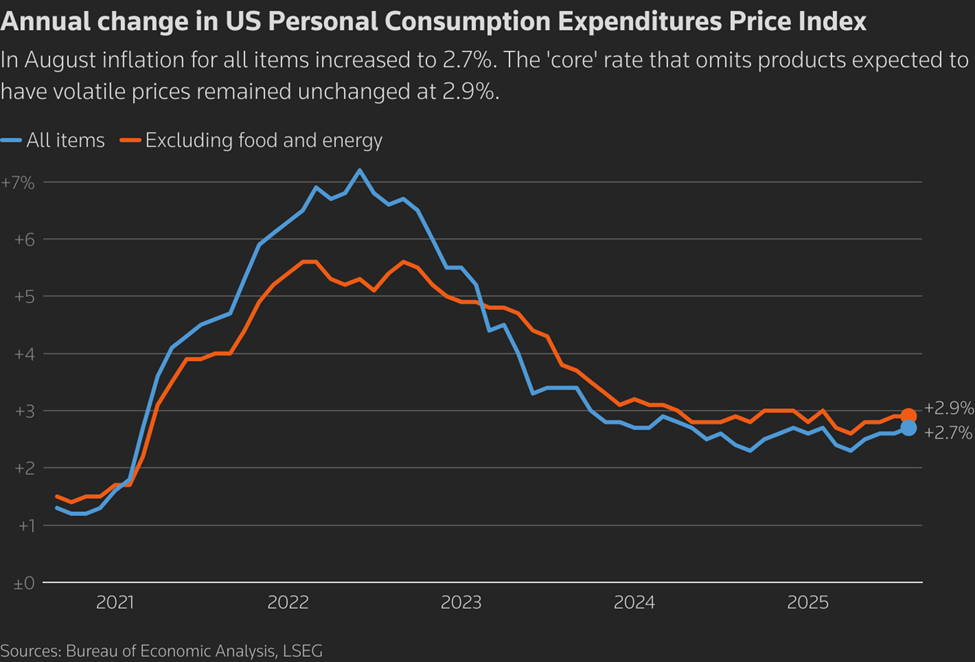

The U.S. remains the anchor for global risk sentiment. August’s personal consumption expenditures (PCE) index rose 0.3% month-over-month and 2.7% year-over-year, with core PCE holding at 2.9%.

This stability, though above the Federal Reserve’s 2% target, suggests inflation is contained rather than re-accelerating. The Fed’s recent quarter-point rate cut was a nod to growth concerns, but policymakers remain clear: they are walking a tightrope. Richmond Fed President Tom Barkin underscored that risks to both inflation and jobs “may be limited,” but the central bank must remain data dependent. (Source: Trading Economics)

Earnings Edging Higher

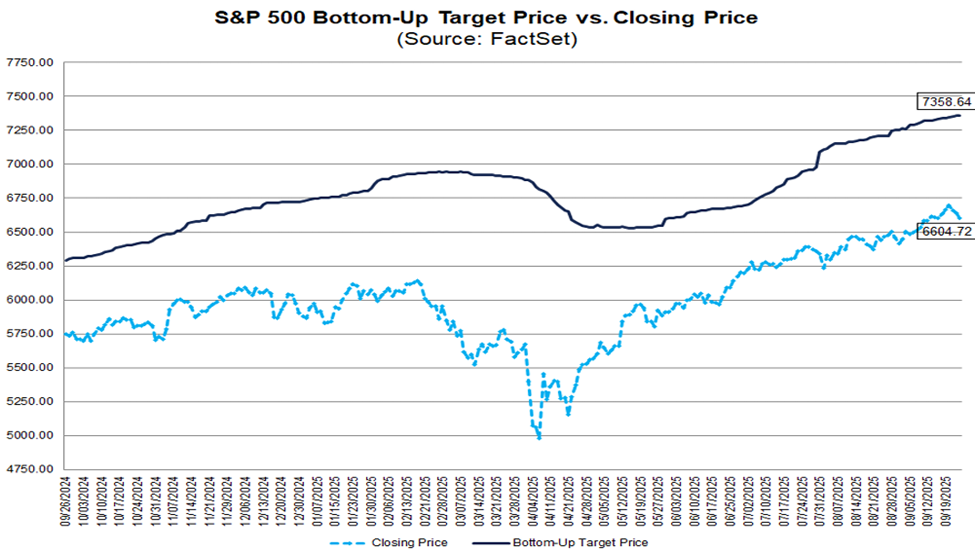

Industry analysts are projecting solid gains for the S&P 500 over the next year, with an aggregate forecast calling for an 11.4% price increase. This estimate is based on the “bottom-up” target price the sum of company-level median price targets set by analysts for each stock in the index. As of September 25, that target stood at 7,358.64, compared with the index’s closing value of 6,604.72. At the sector level, Health Care is expected to lead with a potential 15.5% upside, while Communications Services shows the smallest increase at 7.5%.

This outlook comes against a backdrop of steady improvement in analyst expectations since the spring. After dipping to 6,526.32 on May 14, the bottom-up target for the index has risen by 12.8% over the past four months. Ten of eleven sectors have seen their targets move higher in that time, led by Information Technology with a 23.2% increase. Together, these revisions highlight analysts’ growing confidence in the earnings and valuation support behind the market’s recent record highs.

Tariff Fallout in October

Markets are also preparing for a fresh round of U.S. tariffs set to take effect in October. Heavy trucks, cabinetry, films, pharmaceuticals, and furniture are on the list industries with both domestic and cross-border supply chains. The likely impact: upward pressure on prices, squeezed corporate margins, and possible retaliation from trading partners. While not catastrophic in scale, these measures add to inflation stickiness and complicate the Fed’s policy path. Investors are bracing for earnings calls in Q4 to reveal how management teams plan to navigate higher input costs. (Source: The Guardian and CNN)

U.S. Labour and Consumers: Resilient but Diverging

The labour market has softened at the margin, with job growth slowing, but unemployment remains historically low. Wages continue to climb, supporting consumption though lower-income households are showing early signs of strain, particularly in discretionary categories. Still, consumer spending represents nearly 70% of U.S. GDP, and even modest resilience here provides a floor for growth. Holiday shopping season trends will be pivotal in determining whether the U.S. economy continues to expand at a modest pace or slips into stall speed.

Canada: Divergence, Resources, and Housing Pressures

A Surprise Rebound in Growth

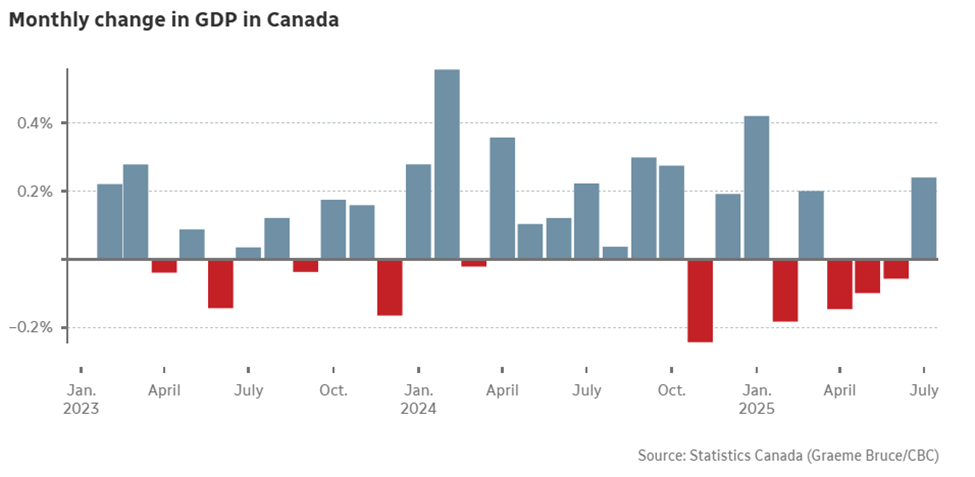

Canada entered fall with a modest but welcome GDP rebound: July growth came in at +0.2% after three straight months of contraction. Gains in oil & gas, mining, and manufacturing led the way, offsetting weakness in housing and construction. This data point reassured investors that Canada’s economy retains resilience despite heavy household debt loads and a fragile consumer sector. (Source: CBC)

Housing Headwinds Continue

The Canadian real estate market, particularly in Toronto and Vancouver, is showing signs of strain beneath the surface despite headline resilience. Elevated interest rates have sharply eroded affordability, leaving buyers on the sidelines and forcing many households into stretched debt-service ratios. In Toronto, the pre-construction condo market is under stress: investors who bought units at peak valuations in 2021–2022 are now facing negative cash flows as rents fail to cover higher mortgage payments, while assignment sales (reselling pre-construction contracts before closing) are increasingly being listed at discounts. Mortgage renewals are another fault line households rolling over from ultra-low pandemic rates to 5–6 % terms are seeing monthly payments jump by hundreds or even thousands of dollars, which risks adding forced sellers to a market already carrying elevated inventory.

In Vancouver, the underbelly is even more exposed to external shocks. The city’s market has long leaned on foreign capital and speculative demand, but tighter capital controls in China, federal anti-money-laundering scrutiny, and higher taxes on non-resident ownership have slowed offshore inflows. At the same time, supply pipelines are starting to weigh multi-family completions are adding inventory at a time when demand is muted, creating localized price softness. Investors who once counted on rapid appreciation are recalculating, while developers are delaying or cancelling projects due to cost inflation and weaker pre-sales. The result is a market where headline averages may mask deeper stress with certain neighborhoods, product types (like small condos), and highly leveraged owners facing outsized downside risk, while liquidity slowly drains out of Canada’s most expensive real estate hubs.

Yet, even as these pressures weigh on Toronto and Vancouver’s markets, there are constructive signals worth noting. Population growth, driven by immigration and interprovincial migration, continues to underpin long-term housing demand, especially in major job hubs. Rental markets remain exceptionally tight, providing investors with steady income opportunities despite softer resale prices. For end-users, the recent cooling is also resetting the playing field: buyers who were previously priced out are starting to see more negotiating power, longer days on market, and a wider range of options. If interest rates ease into 2026 as many forecasters expect, the combination of improved affordability and structural demand fundamentals could stabilize prices and lay the groundwork for a healthier, more balanced housing market in Canada’s two largest cities. (Source: CBRE, CMHC, BMO Canadian Housing Monitor)

Resource Strength as a Bright Spot

Against these headwinds, resources have been a standout. The TSX has gained more than 16% year-to-date, outpacing the S&P 500, thanks largely to gold miners, energy producers, and base-metal exporters. With global investors hedging inflation and geopolitical risk through hard assets, Canada’s heavy weighting toward natural resources has proven a structural advantage. Rising demand for copper, nickel, and gold coupled with energy’s ongoing role in powering AI data centers and global trade supports the case for sustained outperformance in Canadian resource equities. (Source: CBC, Bloomberg)

Energy Transition and Infrastructure

The energy transition is not just a buzzword. It’s showing up in real projects and shifting trade flows. A prime Canadian example is the Trans Mountain Expansion (TMX), which came online in 2024. This project nearly tripled the pipeline’s capacity to 890,000 barrels per day, and it is already running close to full utilization. YTD 2025 guidance cites ~84% average utilization, with potential to max out around 2027–2028. Pipeline shipments from Alberta to British Columbia jumped over 400% compared to pre-expansion levels (Source: CER & StatCan).

The big shift? Canada now has direct access to Asian buyers. China, for example, has quickly become the top purchaser of TMX crude, taking more than 200,000 barrels a day in some months (Source: Reuters). For investors, this means Canadian producers are no longer entirely dependent on U.S. refiners, which is a major diversification win at a time of trade friction.

Meanwhile, both Canada and the U.S. are spending heavily on infrastructure tied to the energy transition. This includes LNG export terminals, power-grid upgrades, and supply chains for critical minerals. For companies in construction, heavy machinery, and clean energy, these investments represent multi-year growth tailwinds that go well beyond quarterly market swings.

Geopolitical Overlay

Geopolitics is no longer a background feature. it’s an active driver of capital flows, trade alignments, and industrial strategy. The U.S.-China frictions, especially around semiconductor technology and dual-use inputs, have raised the cost of complacency in supply chains. As Washington tightens export controls on advanced computing equipment, Beijing has responded by restricting exports of certain high-tech materials, triggering ripples across global value chains. These tensions are reanimating a new industrial geometry: alliances and trust are becoming as important as raw cost in deciding where chips, batteries, and magnets get built. (Source: CNN, DiscoveryAlert)

For Canada, this shift is a tailwind more than a headwind. With abundant nickel, rare earth, lithium, and other critical minerals, the country is increasingly viewed as a stabilizing partner in North American and allied supply chains. Ottawa’s ongoing coordination with U.S. agencies including under the Canada-U.S. Joint Action Plan for Critical Minerals signals that downstream investment is no longer a theoretical ambition but a policy priority. The U.S. Department of Defense has already used its investment tools (e.g., elements of DPA Title III) to jump-start critical mineral projects in Canada, opening the door to shared incentives and joint capacity building. (Source: CSIS)

For investors, this triangulation of strategy, resource endowment, and geopolitical trust offers compelling runway. Yes, shocks remain — sudden tariff shifts or sanctions could rattle markets temporarily, but the broader arc is clear: North America’s shared infrastructure, regulatory predictability, and resource depth position Canada and the U.S. as anchor suppliers in the evolving clean energy and tech order. Whether it’s battery metals, rare earth magnets, or semiconductor grade inputs, Canadian firms now have a chance not just to ride the wave of demand but to help shape it.

In Summary

Even with challenges like tariffs and stubborn inflation, markets still have reasons to move higher. Company earnings have held up better than expected, with many businesses managing costs well and keeping profits steady. At the same time, central banks have started shifting toward small rate cuts, which makes borrowing cheaper and helps boost confidence. Together, these trends give stocks a solid base to keep climbing as we head into the last quarter of the year. Looking past the short-term headlines, bigger forces are working in favor of the market. Canada’s resource sector is seeing strong demand for energy, gold, and critical minerals, while in the U.S. heavy investment in technology and infrastructure is fueling growth. The push toward clean energy, the boom in data centers, and the reshaping of supply chains are all creating steady demand that goes beyond this quarter or even this year. These long-term shifts give investors real opportunities to stay invested with confidence.

Of course, risks haven’t disappeared. Canada’s housing market, high household debt, and the chance of more trade tensions could create bumps along the way. But history shows markets often rise even while worries remain in the background. By focusing on quality companies and key growth areas, investors can benefit from the upside while staying mindful of potential risks. With steady earnings, strong demand for resources, and supportive trends in place, the outlook for a continued rally into year-end remains encouraging.

We thank you for your continued trust and we welcome you to reach out to us with any questions you may have.

This information has been prepared by Kian Ghanei and Terry Fay who are Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.