Resilience with a Dash of Realism

As we wrap up November, markets are trying their best to finish the year on a constructive note, even if it feels at times like we’re driving with one foot on the gas and one hovering over the brake. The economic data on both sides of the border has been encouraging, earnings have remained stronger than expected, inflation continues to cool in a generally orderly manner, and labour markets are loosening just enough to ease central bankers’ nerves without breaking confidence. Still, it wouldn’t be 2025 without a little noise. Tariff tensions, affordability pressures, political recalibrations, and shifting growth expectations all contributed to a market tone that is cautiously optimistic, but not naive.

Labour Markets: Cooling Just Enough

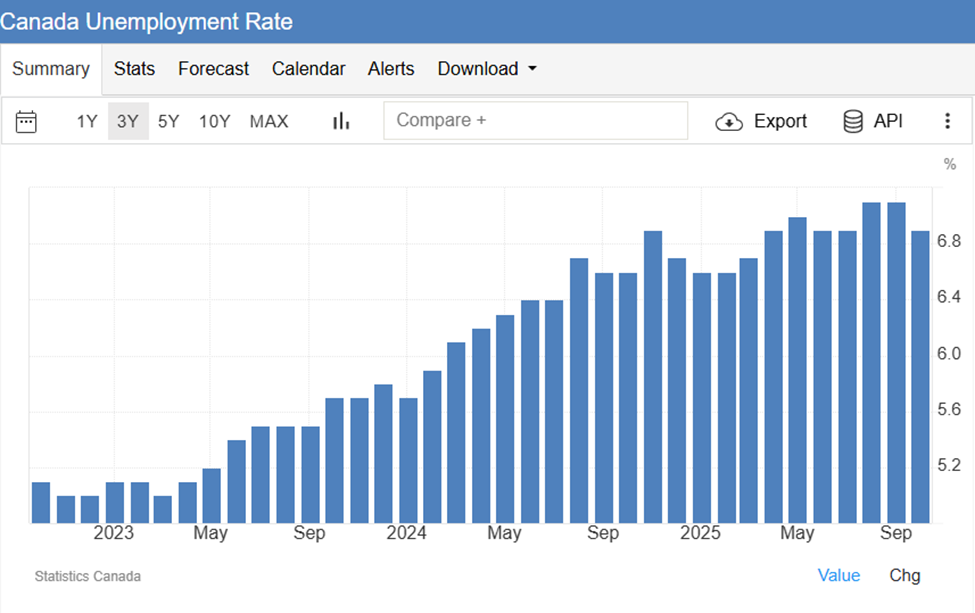

Labour data in both Canada and the United States continues to soften in a way that indicates normalization rather than deterioration. In Canada, the unemployment rate has ticked higher to 6.9% through the fall as population growth outpaces job creation, though the labour market remains historically strong and continues to shift in the direction the Bank of Canada wants to see as it moves toward a more dovish stance. (Source: Statistics Canada)

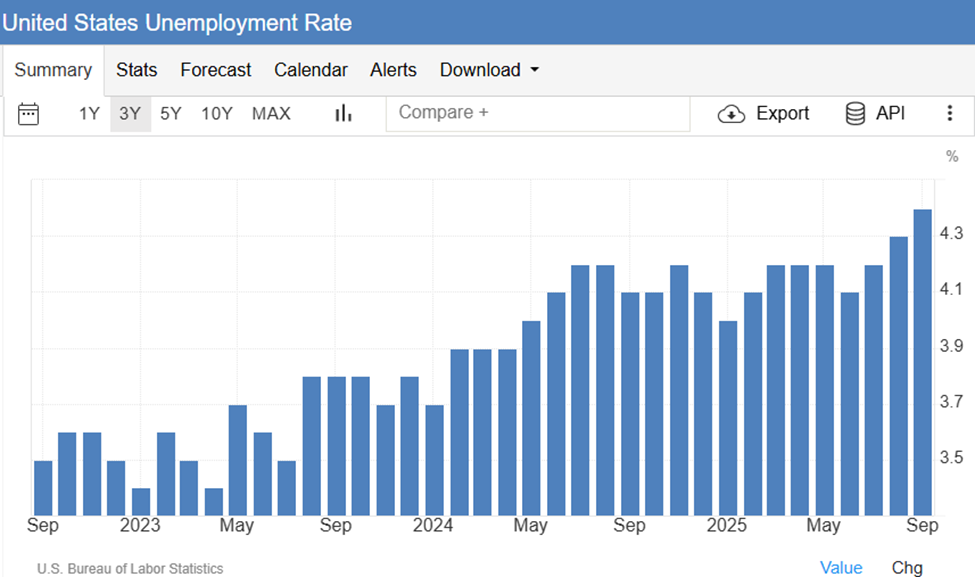

In the U.S., unemployment has also crept up modestly from cycle lows to 4.4% in early fall pointing to a gradual increase over the last 2 years. (Source: US Bureau of Statistics)

Job openings have cooled, wage pressures have eased, and together these trends give the Federal Reserve the breathing room it needs to transition from “higher for longer” toward a more patient “hold and assess” posture. From a market perspective, both countries are showing a labour-market slowdown that reduces the risk of inflation re-acceleration while maintaining enough underlying momentum to support corporate earnings.

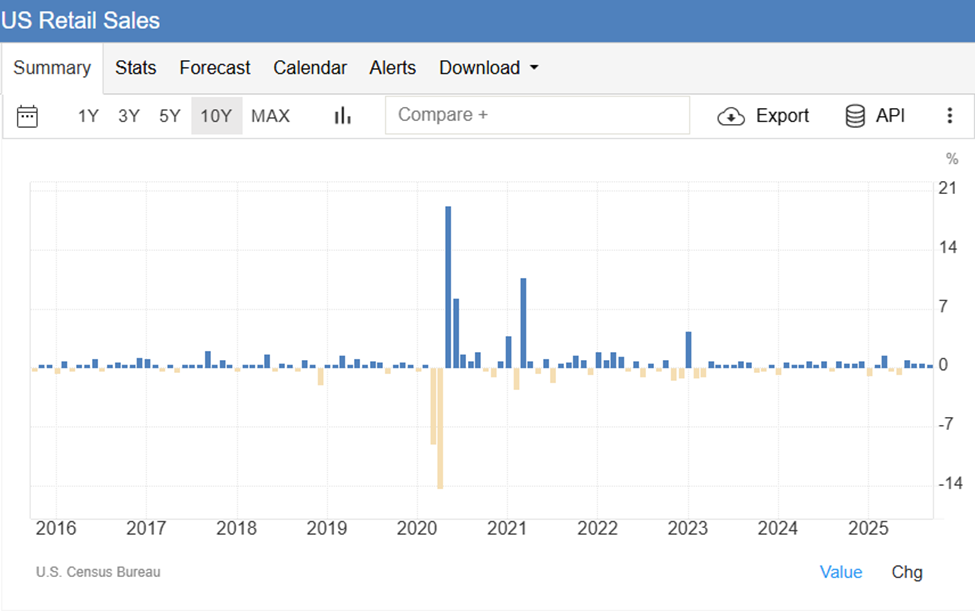

Consumer Spending & Retail Sales: Still Holding Up

Despite frequent headlines about strained households, actual spending behaviour continues to demonstrate resilience. In Canada, the latest retail spending data from Statistics Canada shows stable, though uneven, growth across several key categories. (Source: Statistics Canada)

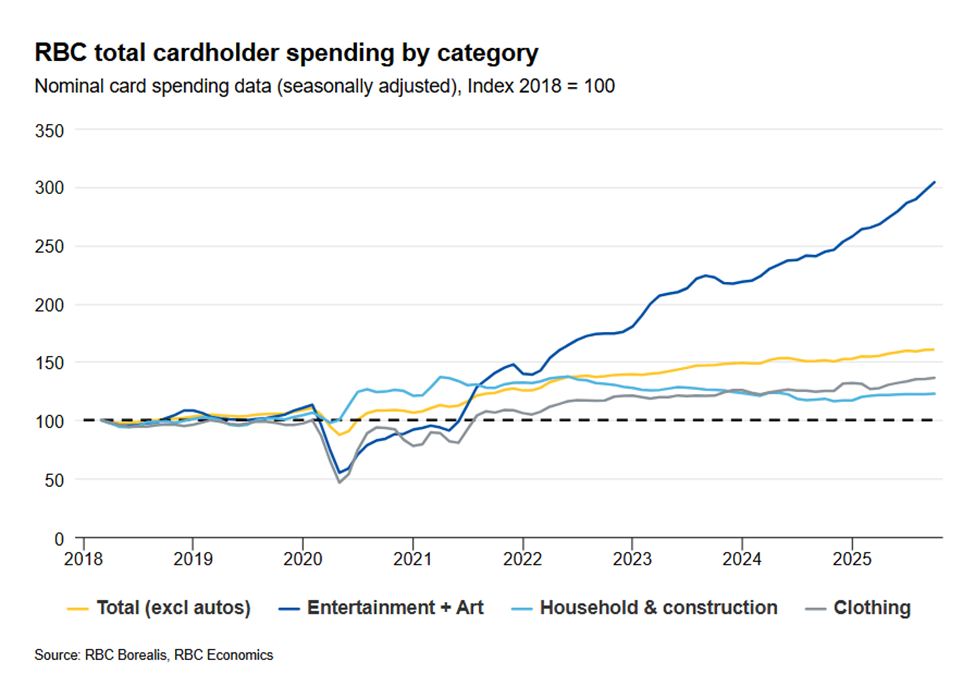

RBC’s Consumer Spending Tracker reinforces that trend, illustrating that while discretionary purchases have cooled, essential spending and services remain solid. Canadians are being more selective, but they have not pulled back in a meaningful way. Although this is data from one bank alone, it further confirms the data of Stat Can. (Source: RBC)

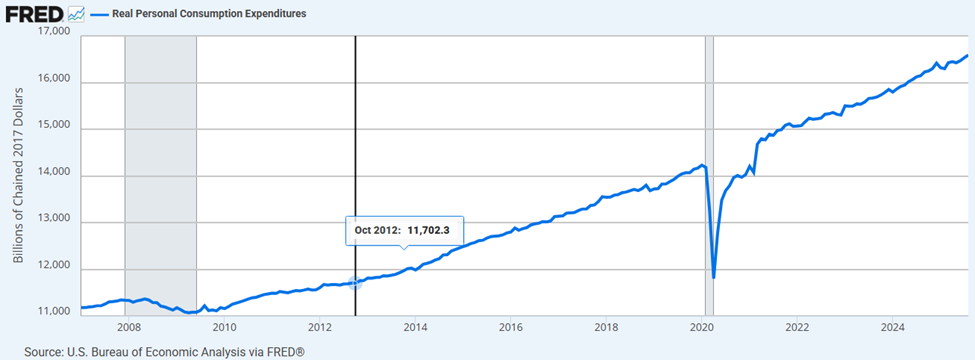

In the United States, consumer spending continues to be one of the strongest drivers of the economy. Inflation-adjusted personal consumption expenditures remain firm, indicating that Americans continue to lead global demand. (Source: US Bureau of Economic Analysis via FRED)

Furthermore, retail sales, while moderating in select categories, remain well above pre-pandemic levels and demonstrate that consumers are still very much engaged.

Overall, both countries show a similar pattern. Consumers may be stretched, but they are not tapped out. Strong wage trends, easing inflation, and still-healthy labour markets are keeping spending afloat, though elevated interest rates and rising credit usage remain areas to watch.

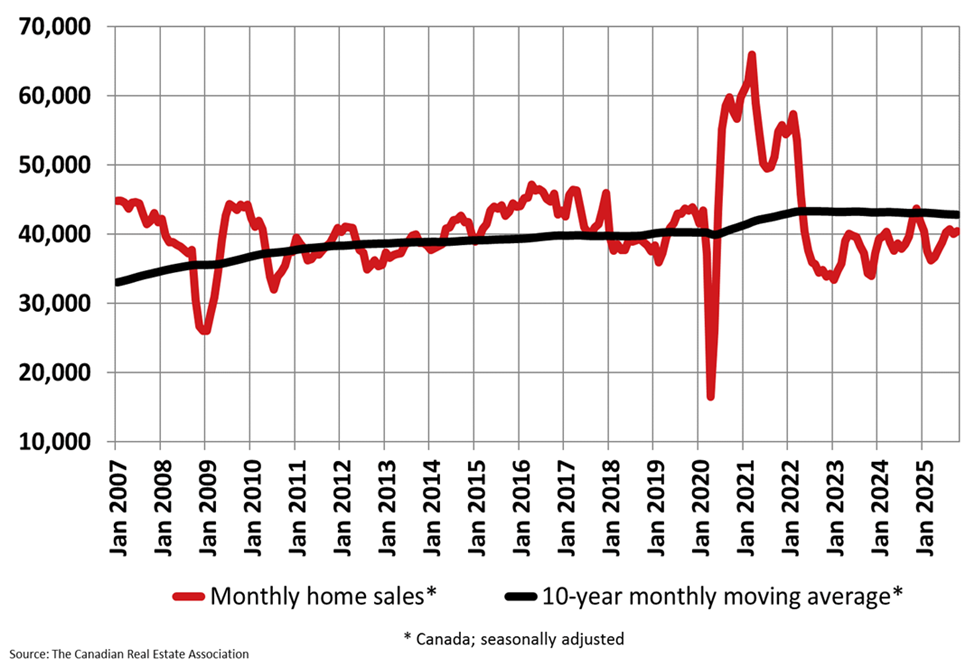

Housing Supply & Rental Costs: Finally, Some Cooling

Housing remains one of Canada’s most closely watched economic variables, and for good reason. After several years of relentless increases, rents in major cities, including Vancouver, are finally beginning to decline as new supply enters the market. This cooling in the rental market provides modest but meaningful relief for households and contributes positively to the inflation backdrop.

(Source: The Vancouver Sun)

With real estate sales down nearly 14% year over year, Vancouver home prices too have experienced some price softening. The lower sales activity isn’t surprising given the last two years of above average interest rates and is seen across the country. (The Canadian Real Estate Association)

National home prices, meanwhile, have stayed surprisingly resilient, buoyed by population growth and persistent supply shortages, though month-to-month volatility has increased. There are however some that believe that the real estate market is showing signs of a rebound as interest rates continue their downward direction. “As we head into the quiet winter season, we continue to see clues that underlying demand for housing is picking up steam,” said Valérie Paquin, CREA Chair. “All eyes will be on next year’s spring market to see if all that pent-up demand will finally come off the sidelines in a big way.” (Source: CREA)

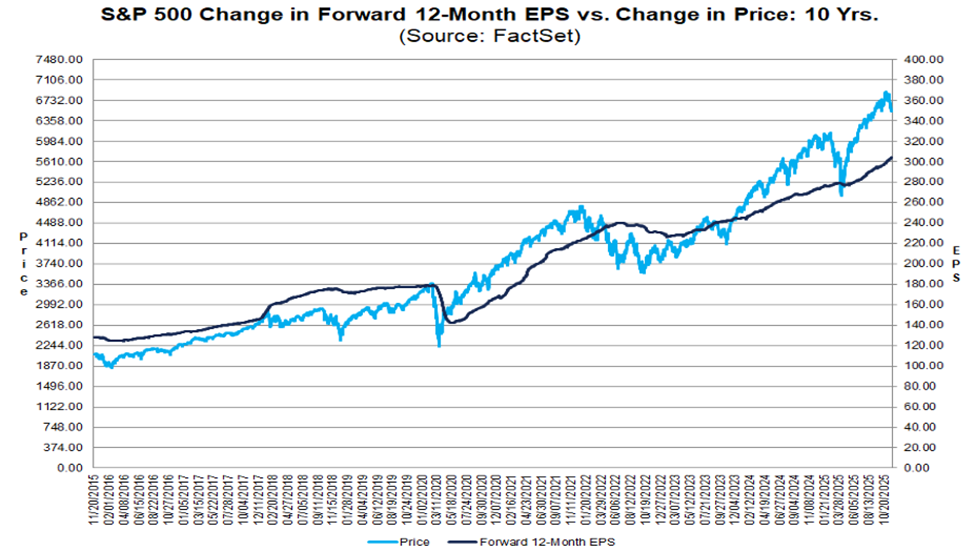

Earnings Continue to Drive Long-Term Market Gains

Despite periodic bouts of volatility, corporate earnings remain one of the strongest pillars of the 2025 market story. Companies across Canada and the U.S. have exhibited strong discipline by managing costs carefully, maintaining margins, and continuing to invest in innovation even as higher rates reshape capital-allocation decisions.

Corporate earnings, not headlines, drive long-term market returns. This year, earnings have continued to surprise to the upside. Technology, financials, and industrials have shown leadership, while previously challenged sectors like consumer discretionary are beginning to stabilize. The overall environment continues to support a cautiously optimistic equity outlook heading into 2026.

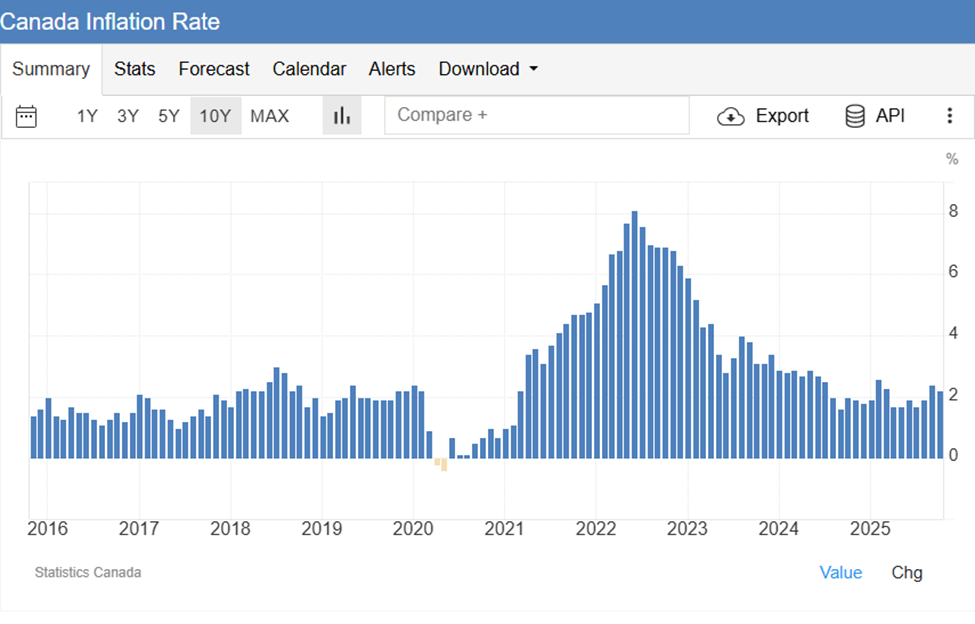

Inflation: Still an Important Piece

Inflation continues to moderate across Canada and the United States, though progress has not been uniform. In Canada, CPI has steadily eased, supporting expectations for possible Bank of Canada rate cuts in 2026. Categories such as energy, food, and shelter have shown mixed movements, but the general direction remains encouraging at 2.2%. (Source: Trading Economics & Stats Canada)

In the U.S., inflation is also trending lower, though shelter costs remain somewhat sticky. Even so, the Federal Reserve has expressed increasing confidence that inflation is returning toward its 2% target. For now, inflation is stubbornly hovering around 3% which really isn’t surprising given the robust consumer spending mentioned above. However, with unemployment ticking higher, the odds of a rate cut by the Federal Reserves is becoming more likely over the next few months.

Strains for Canada Remain: Debt, Tariffs, and Provincial Tensions

Canadian household debt continues to push into record territory, now exceeding $2.6 trillion, as borrowing costs begin to ease and credit usage ticks higher. While this debt load remains a clear macro-vulnerability, particularly after two years of elevated interest rates, the anticipated shift toward lower rates in 2026 should offer some relief. The key stabilizer will be wage growth: if incomes continue to rise at a pace that offsets inflation and debt-servicing costs, household balance sheets may gradually regain resilience. (Source: Wealth Professional & TransUnion)

Trade policy added further complexity in November, with Ottawa rolling out additional supports for steel and lumber producers affected by ongoing U.S. tariff actions. These measures underscore the continued fragility of Canada’s export environment, where competitive pressures, geopolitical bargaining, and sector-specific tariffs intersect. Although the federal response aims to cushion near-term impacts, it also highlights the importance of diversifying markets and expanding infrastructure capacity, particularly as global demand shifts toward Asia and non-U.S. supply chains. (Source: Reuters)

Meanwhile, interprovincial tensions resurfaced as British Columbia openly challenged Alberta’s renewed push for expanded pipeline corridors, dismissing certain proposals as “distractions from real projects.” While these disputes are unlikely to create immediate market risk, they reflect a deeper structural challenge: Canada’s inability to fully align provincial ambitions with a cohesive national energy and economic framework. As regions prioritize their own political and economic objectives, the friction complicates long-term competitiveness and underscores the need for more coordinated, future-focused national planning. (Source: CTV News Vancouver)

Summary

If November had a tagline, it would be: “We’re doing better than the headlines suggest.” Labour markets are cooling but nowhere near collapsing. Consumers are adjusting their spending habits but not retreating from the marketplace. Housing is showing just enough loosening, particularly in rents, to help inflation without undermining sentiment. Corporate earnings continue to perform and provide critical support to market stability. Inflation is behaving more consistently, and central banks are edging closer toward rate cuts. Canada’s structural strains, while real, are manageable. And yes, tariffs, political theatrics, and provincial disagreements continue to add colour.

All told, the tone heading into December is one of cautious optimism. The environment is not exuberant, nor is it fearful. It is realistic, anchored in data, supported by earnings, and attentive to the risks that remain. Markets may wobble and the path ahead may twist, but the economic foundation is stronger than many expected. And in a year like 2025, that’s something worth appreciating.

We thank you for your continued trust and we welcome you to reach out to us with any questions you may have.

This information has been prepared by Kian Ghanei and Terry Fay who are Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.