January opened with a familiar mix of confidence and complexity for global markets. Economic data continues to suggest that growth in North America remains resilient, inflation is trending lower, and corporate earnings are holding up better than many feared just a year ago. At the same time, investors are being asked to navigate a landscape shaped by geopolitical negotiation, shifting trade alliances, evolving central bank policy, and notable moves in currencies and commodities. The result is an environment that rewards patience and selectivity rather than broad, uncritical risk-taking. As we move deeper into 2026, the tone remains cautiously optimistic, supported by improving fundamentals but tempered by policy and political uncertainty that can quickly reshape market sentiment.

Geopolitics and trade have been front and center this month, as Canada works to reset its relationship with China amid broader U.S. efforts to maintain strategic and economic influence. Prime Minister Mark Carney’s visit to Beijing, the first in several years, produced a targeted trade framework rather than a full agreement. The agreement is best understood as a normalization effort rather than a sweeping realignment. It reflects a mutual interest in stabilizing trade flows and restoring dialogue in sectors such as agriculture and energy, without committing either side to a full-scale free trade framework. Although some may find this development unwelcoming, most Canadian in the post-tariff era are open and encouraged by the new agreement.

However, the reaction from the United States has underscored how sensitive the broader North American trade environment remains. The Trump administration has warned that a more comprehensive Canada–China trade deal could prompt retaliatory measures from Washington, including the possibility of sharply higher tariffs on Canadian goods by as much as 100%. U.S. officials have framed their concerns around supply chain integrity, arguing that even limited tariff relief for Chinese electric vehicles could create a “back door” into the North American market, potentially disadvantaging U.S. manufacturers and workers. These statements are also occurring against the backdrop of the upcoming review of the USMCA trade agreement, where the United States is widely seen as seeking leverage for broader concessions.

(Sources: Reuters; Bloomberg; Government of Canada – Global Affairs Canada)

The Gold Rush

Another notable feature of January has been renewed attention on gold and precious metals, driven in part by broader discussions around fiscal sustainability and long-term inflation risk. When government debt levels and deficits rise, markets often begin to question how much flexibility central banks truly must keep interest rates elevated without creating stress elsewhere in the system. Higher interest expenses for governments, political pressure to support growth, and the potential fragility of heavily leveraged sectors can all contribute to a perception that policy may eventually need to lean more accommodative. This does not mean that central banks are poised to abandon their inflation-fighting mandates, but it does influence how investors think about long-term purchasing power and the role of non-fiat assets in portfolios.

The World Gold Council has pointed directly to U.S. fiscal dynamics and debt sustainability as a supportive backdrop for gold demand. As bond markets become more sensitive to the trajectory of government borrowing, the risk premium attached to long-term inflation and currency debasement can rise. In that context, gold often benefits as a form of monetary hedge rather than a simple inflation trade. For investors, the renewed interest in gold serves as a reminder of its function as a diversifier and a potential stabilizer during periods of policy uncertainty.

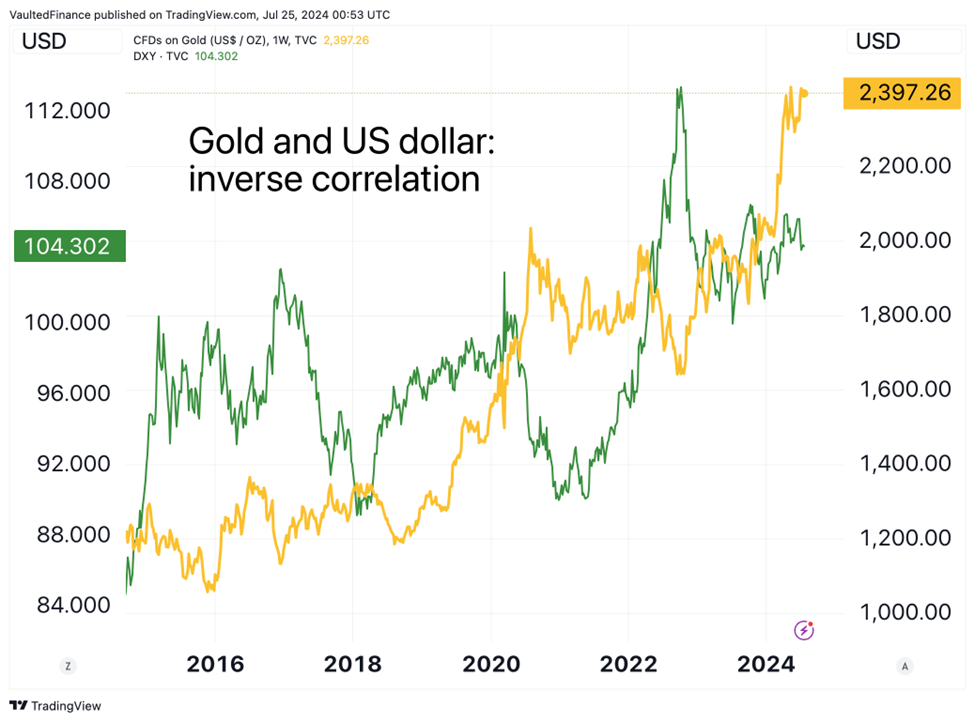

Another way to explain the run up in the price of gold may be pegged to the US dollar. When the U.S. dollar weakens, gold often becomes more attractive to buyers outside the United States because it effectively becomes “cheaper” in their local currencies. This can increase global demand and help support higher gold prices. When the dollar strengthens, the opposite tends to occur, as gold becomes more expensive for international buyers, which can temper demand. In fact, gold had a major pullback on Friday Jan 30th as USD strengthened against other currencies.

Gold’s broader relationship with the dollar also reflects where most demand comes from. A significant share of global gold buying is driven by investors, consumers, and central banks outside the U.S., particularly in countries such as India and China, where gold plays an important cultural and financial role. In recent years, several major central banks, including those in China, Russia, and India, have increased their gold holdings as part of efforts to diversify reserves and reduce reliance on the U.S. dollar, reinforcing gold’s role as a long-term store of value in the global financial system.

(Sources: World Gold Council (gold.org); Federal Reserve Bank research publications)

U.S. Dollar

As expectations for future Federal Reserve policy have become more nuanced, some of the yield advantage that supported the dollar in prior years has narrowed. At the same time, global investors have been actively managing their exposure, hedging or reducing dollar positions as part of broader diversification strategies.

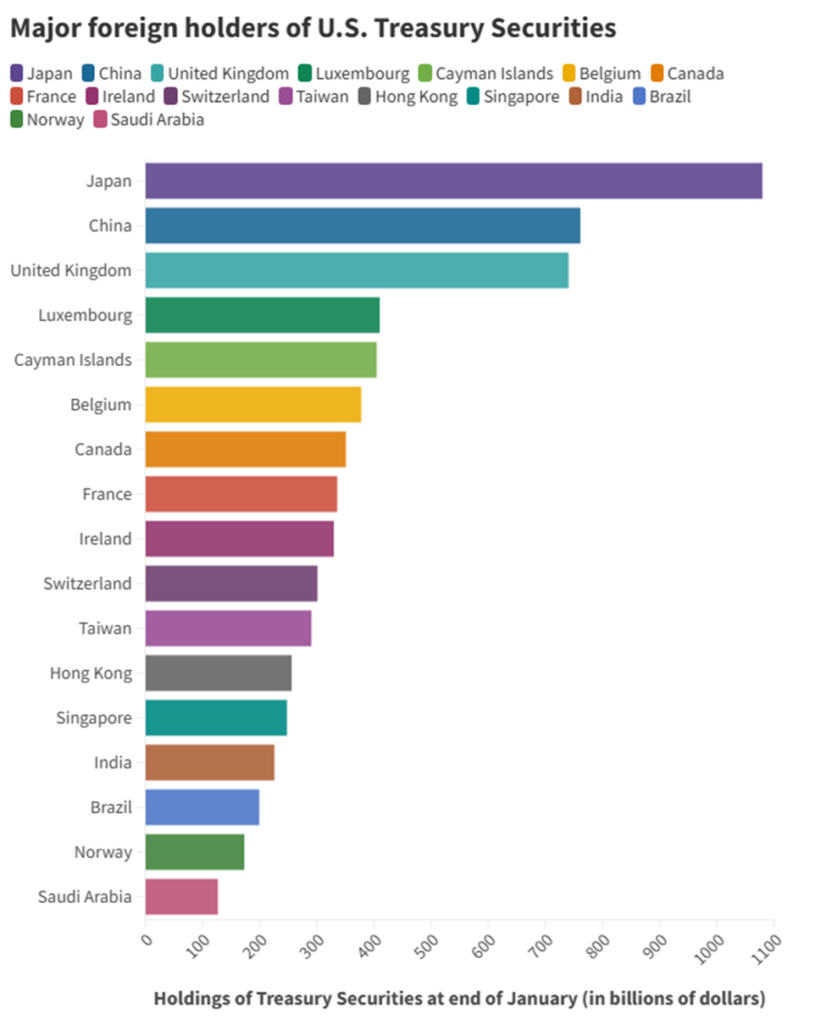

At the national level, several large foreign holders of U.S. Treasuries have been gradually trimming their reserves. Countries such as China, India, and Brazil have reduced their holdings as part of longer-term efforts to diversify reserves, often reallocating toward gold or other currencies. Japan, while still the largest foreign holder of U.S. government debt, has also experienced periods of net selling as it manages its own currency and yield dynamics. Importantly, these actions do not amount to a coordinated “dump” of Treasuries. Overall foreign ownership remains near record levels, reflecting continued demand from other sovereign and global investors.

Institutional behavior, particularly in Europe, has added another layer to the narrative. Several large pension funds and asset managers have publicly reduced their exposure to U.S. government bonds, citing concerns about fiscal policy risk and the desire for greater portfolio diversification. In Sweden, for example, major pension funds have shifted allocations toward domestic bonds and alternative assets. Similar patterns have been observed among Danish and broader European investors. These moves are driven by portfolio management considerations rather than government policy, but collectively they have contributed to the perception of increased selling pressure in parts of the Treasury market and, by extension, to the recent softness in the dollar.

(Sources: U.S. Department of the Treasury – TIC Data (home.treasury.gov); Reuters; Bloomberg)

Inflation Trends

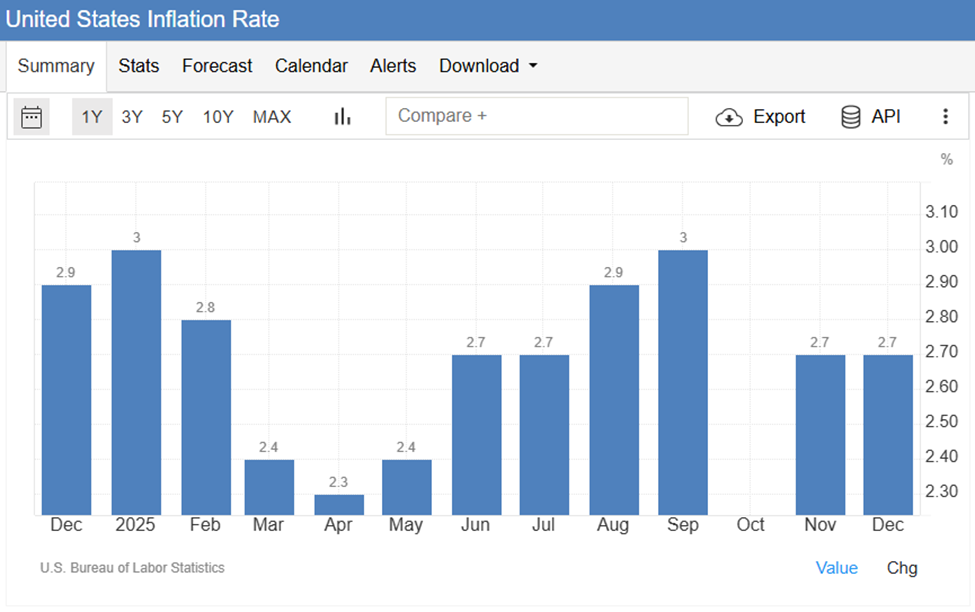

Inflation data on both sides of the border continues to support the view that price pressures are moderating, albeit unevenly. In the United States, the annual inflation rate held steady at 2.7 percent in December, in line with market expectations. Energy prices were a key source of relief, with gasoline prices declining and fuel oil inflation easing, while natural gas prices rose more sharply. Used car and truck prices also showed slower growth. Offsetting these trends, food and shelter costs accelerated modestly, reminding policymakers and investors alike that services inflation remains a persistent challenge. Core inflation, which strips out food and energy, remained at 2.6 percent, the lowest level since 2021, and below expectations for a slight increase. On a monthly basis, headline inflation rose 0.3 percent, driven largely by shelter costs, while the core measure came in softer than forecast.

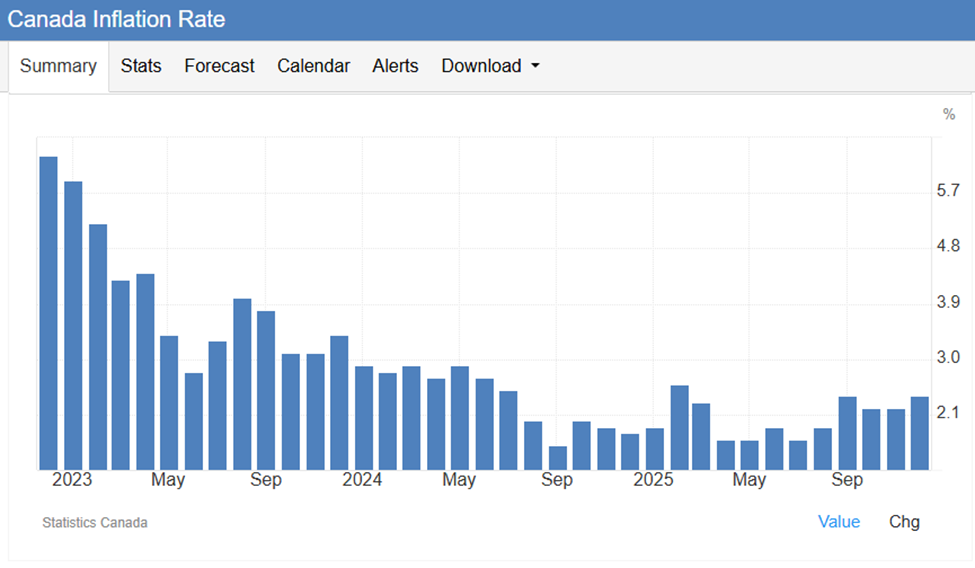

In Canada, inflation ticked higher to 2.4 percent in December, up from 2.2 percent in November and above market expectations. The increase was influenced in part by base effects related to the temporary GST and HST break introduced in December of the prior year. Categories such as restaurant food, alcoholic beverages, and recreational goods saw sharper price increases as those tax measures rolled off. At the same time, shelter inflation eased and transportation prices declined. The Bank of Canada’s closely watched median core inflation measure slowed to a one-year low of 2.5 percent, suggesting that underlying price pressures are still trending in a favorable direction despite the headline uptick.

(Sources: U.S. Bureau of Labor Statistics (bls.gov); Statistics Canada (statcan.gc.ca))

Central Banks in Focus

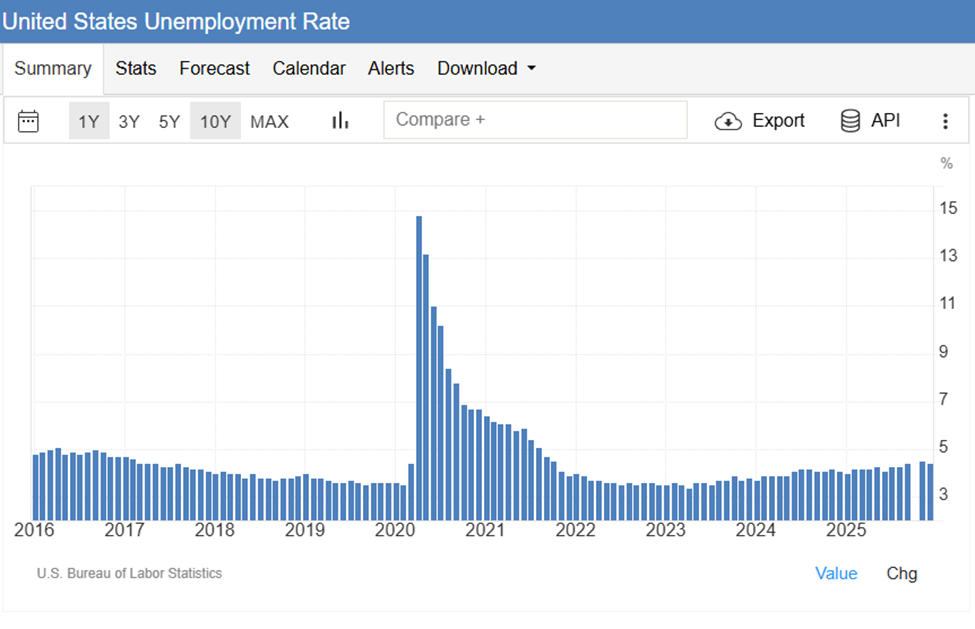

Central bank policy remains a central pillar of the market outlook. The Federal Reserve’s late January meeting resulted in no change to the federal funds target range, which remains at 3.50 to 3.75 percent. This decision marked a pause after a series of rate cuts late last year and reflected the Fed’s assessment that the U.S. economy continues to grow at a solid pace, inflation remains above the 2 percent target, and the labor market is stabilizing. The US unemployment rate edged down to 4.4% in December 2025, from a revised 4.5% in November, which had marked the highest level since October 2021. The reading also came in slightly below market expectations of 4.5%.

Fed Chair Jerome Powell underscored that the current stance of policy is designed to balance the dual mandate of maximum employment and price stability. He reiterated that future decisions will be data-dependent rather than guided by a preset path.

The Bank of Canada has adopted a similarly cautious posture. At its January decision, the Bank held its policy rate steady at 2.25 percent, with Governor Tiff Macklem emphasizing that while inflation is easing, the outlook remains uncertain. Global economic conditions and trade risks were cited as reasons for maintaining a data-dependent approach. The next policy decision in March will provide an opportunity to reassess the balance between growth and inflation in light of evolving domestic and international developments.

(Sources: Federal Reserve – FOMC Statement and Press Conference (federalreserve.gov); Bank of Canada (bankofcanada.ca))

Corporate Earnings & Market Leadership

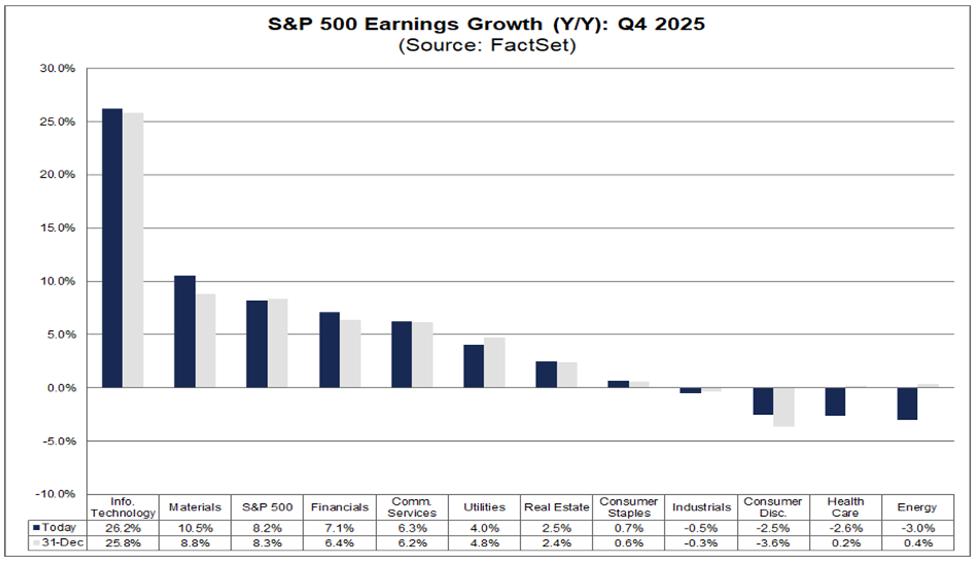

Against this macroeconomic and policy backdrop, corporate earnings have provided a constructive, if uneven, foundation for market confidence. In the United States, fourth-quarter reporting is tracking toward approximately 15 percent year-over-year earnings growth on about 8 percent higher revenues, according to FactSet. This performance reflects another quarter of solid profitability for the S&P 500, with technology and materials sectors leading the upside. Companies tied to artificial intelligence, automation, and industrial investment have frequently exceeded expectations, highlighting the continued strength of capital spending and innovation-driven demand.

At the same time, sector dispersion remains pronounced. More cyclical areas, such as energy and certain segments of consumer discretionary, have reported weaker results or year-over-year declines. Health care and insurance companies have faced policy-related headwinds that have weighed on margins and guidance. High-profile bellwethers in logistics and transportation, including major parcel and freight operators, have delivered stronger-than-expected results, helping to bolster overall market sentiment. The S&P 500’s ability to trade near record highs in this environment reflects both the strength of leading sectors and investor confidence in forward earnings potential.

In Canada, the earnings picture has been more concentrated, with the financial sector playing a central role. Major banks, including Royal Bank of Canada, TD, and Bank of Montreal, have generally reported strong results, supported by stabilizing credit trends and solid performance in wealth and investment management divisions. Dividend increases have reinforced the sector’s appeal for income-oriented investors. Outside of financials, results have been more mixed, particularly in resource-related industries that remain sensitive to commodity price fluctuations and global demand dynamics.

In Summary

January has opened with a blend of resilience and complexity across global markets. Economic data continues to point to steady growth in North America, easing inflation pressures, and generally constructive corporate earnings, particularly within the technology and financial sectors. At the same time, investors are navigating a backdrop shaped by evolving trade relationships, shifting central bank policy, and notable moves in currencies and commodities, including gold and silver. Canada’s efforts to normalize trade with China, alongside ongoing U.S. concerns around supply chains and strategic influence, highlight how policy and geopolitics remain powerful forces in shaping market sentiment. These dynamics reinforce the importance of staying selective and diversified, as headlines and negotiations can quickly influence specific sectors and regions.

From a portfolio perspective, our decision in 2025 to maintain a stronger weighting in Canada has had a positive impact on overall results and remains well suited to today’s landscape. The relative strength of Canadian financials, more stable domestic inflation trends, and exposure to real assets and commodities have provided both income and balance during a period of global uncertainty. While investment themes can change quickly and 2026 may unfold quite differently than last year, we continue to follow our ADAPT Investment Process to help guide our decisions and see through short-term market noise. We will continue to monitor conditions closely and adjust our positioning as needed, including taking a more defensive stance if warranted. For now, we remain optimistic and continue to benefit from this constructive market environment.

We thank you for your continued trust and welcome you to reach out to our team with any questions you may have.

This information has been prepared by Kian Ghanei, a Senior Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.