It seems the markets got spooked this Halloween as renewed hawkish commentary from Dallas Fed President Lorie Logan tempered expectations for a near-term rate cut, prompting a modest rise in Treasury yields and a repricing of growth-stock valuations. The uptick in yields weighed particularly on high-duration technology names already under pressure from the so-called “AI-capex hangover,” as investors digested heavier infrastructure spending from several megacaps, notably Meta and Microsoft.

In Canada, Prime Minister Mark Carney’s federal budget is set for release on November 4, 2025, marking a shift to an autumn timetable and signaling a blend of austerity and strategic investment. The plan is expected to trim federal operational spending by roughly 15%, scale back certain environmental and transfer programs, and refocus funding toward productivity-enhancing infrastructure, defence, and industrial innovation. Framed as a “budget of discipline,” it aims to restore fiscal credibility while maintaining targeted stimulus for long-term growth, reflecting Ottawa’s attempt to balance fiscal restraint with competitiveness in a slower economic environment.

While these crosscurrents produced near-term volatility, the broader backdrop remains cautiously constructive. Corporate earnings are generally solid, inflation continues to edge lower, and central banks appear closer to the end of their tightening cycle. Together, these dynamics support a patient, selectively risk-on stance, favouring quality balance sheets, reasonable valuations, and diversification while markets adjust to the next phase of the cycle.

Interest Rate Decisions and Underlying Reasoning

In the U.S., the Fed delivered a widely expected 25-basis-point rate cut to its policy range, signalling support for growth while also emphasising that further cuts (including in December) are not assured given lingering inflation concerns and data uncertainty. The statement highlighted that economic activity is expanding moderately, job gains have slowed, and inflation remains somewhat elevated. (Source: federalreserve.gov)

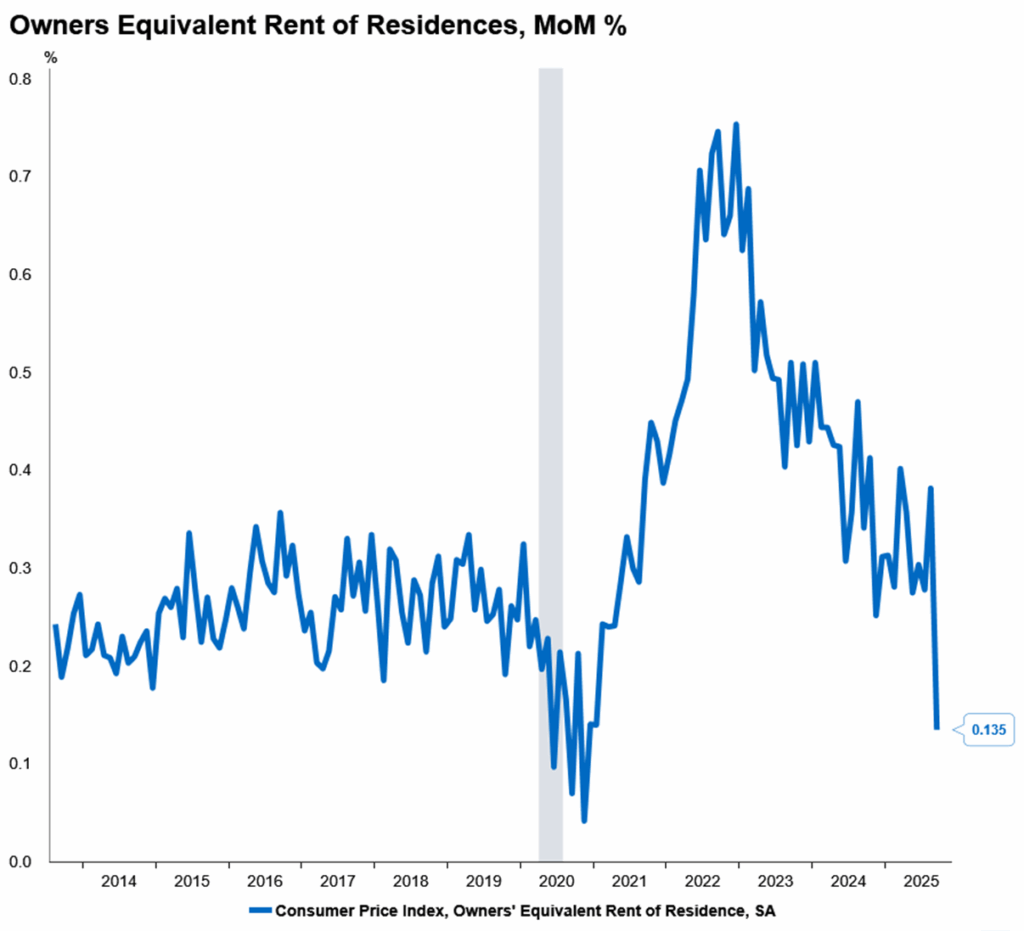

September’s inflation report was a downside surprise, with core and headline inflation coming in below our own expectations and consensus at 3%. The saving grace for the September print was largely the heavily weighted Owners’ Equivalent of Rent (OER) which posted its weakest monthly growth since 2020. (Source: Bureau of Labor Statistics & RBC Economics)

In Canada, the BoC cut its target overnight rate by 25 bps to 2.25 % (Bank Rate at 2.50 %). However, the annual headline inflation rate for Canada rose to 2.4% from 1.9% in August suggesting an uptick in overall prices even with energy prices being modestly low. Some argue that Canada is being pre-emptively cautious around the ongoing tariff negotiations and their prospective fallout.

Bank of Canada governor Tiff Macklem told reporters after the announcement that monetary policymakers feel the key rate is at “about the right level” to keep inflation close to the bank’s two per cent target while supporting the economy through tariff disruptions, provided the economy evolves in line with its forecasts.

Tariffs Update

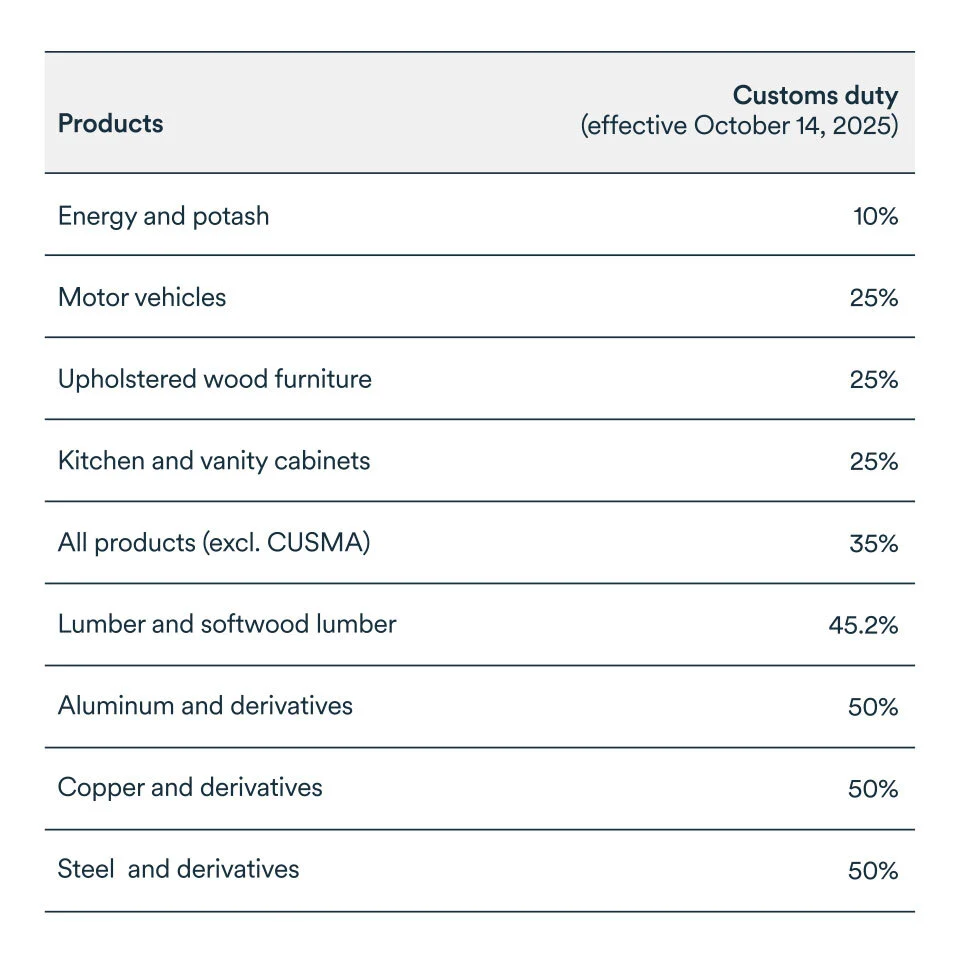

Tariffs may no longer dominate headlines as they did earlier this year, but their impact on the Canadian economy remains both significant and fast-evolving. The trade environment between Canada and the United States continues to shift as new measures are introduced and existing ones are expanded. The most notable recent change has been a broad increase in U.S. tariffs on Canadian goods, rising from 25% to 35% on all products not protected under the Canada–United States–Mexico Agreement (CUSMA).

Fortunately, the trade pact still shields the vast majority (approximately 85% of Canada’s exports to the U.S.) from tariffs. Nonetheless, several key sectors continue to face heavy duties. Automobiles remain subject to a 25% tariff, while steel and aluminum (and products containing them) face a punitive 50% rate. More recently, Washington has widened the list to include new levies of 50% on copper and 45% on lumber, adding fresh pressure to two sectors that are vital to Canadian manufacturing and resource exports.

Further tightening came on July 30, when the White House suspended the long-standing de minimis duty-free exemption. This rule had allowed goods valued under US $800 to enter the U.S. without customs duties, facilitating cross-border e-commerce and supporting thousands of small Canadian exporters. Its suspension has hit small and medium-sized businesses particularly hard, raising costs and complicating logistics for firms that rely on direct-to-consumer sales south of the border.

Tensions between Washington and Beijing eased slightly in late October 2025 following a meeting between President Donald Trump and President Xi Jinping at the APEC Summit in Busan. The two leaders reached a preliminary trade truce, with the U.S. agreeing to lower average tariffs on Chinese imports from roughly 57 % to 47 %, while China suspended certain export-control measures on critical materials and agreed to resume major agricultural purchases—including up to 12 million metric tons of U.S. soybeans this season and a target of 25 million tons annually over the next three years. The White House also paused new port-fee penalties on Chinese-built vessels for 12 months, a move aimed at reducing friction in maritime trade.

Despite the thaw, the new arrangement remains limited, and time bound. Many tariffs still stand at punitive levels, and key structural issues—such as technology access, supply-chain security, and China’s dominance in rare earth exports—remain unresolved. Analysts note that the agreement functions more as a temporary de-escalation than a comprehensive reset: while it may alleviate cost pressures and boost near-term sentiment in global markets, its one-year duration leaves uncertainty high. Overall, the developments mark a modest but meaningful step toward stability in U.S.–China trade relations, offering a short-term reprieve for manufacturers, shippers, and commodity exporters while longer-term strategic tensions continue to simmer.

Consumer Sentiment and Spending Trends in the U.S. and Canada

Consumer behaviour remains a key pillar of growth and market sentiment. In the U.S., consumer expectations for inflation over the next year declined slightly to 4.6 % in October from 4.7 % in September, signalling a modest easing of inflation concerns among households. However, at the same time, a separate report noted that U.S. consumer confidence slipped to a six-month low in October as concerns over job availability rose—especially among lower-income households. (Source: Reuters)

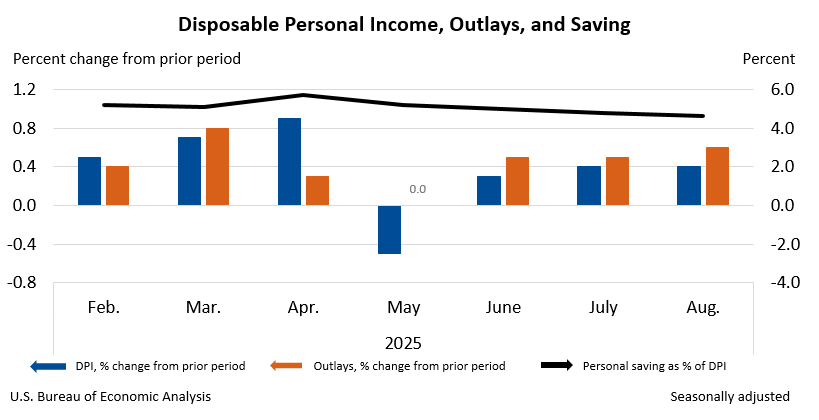

Although there are no official data releases yet for September or October, early indicators suggest that U.S. consumer spending has remained resilient but is showing signs of moderation. The most recent official figure—from August 2025—showed personal consumption expenditures (PCE) rising 0.6% month over month, supported by steady services demand and higher spending among mid- to upper-income households. Federal Reserve district reports through October echoed this trend, describing consumer activity as “modest but stable,” with discretionary categories like travel and dining softening slightly while essentials held firm. Retail trade estimates point to roughly 0.4%–0.5% nominal growth in September, consistent with slower but still positive momentum.

Consumer sentiment in Canada has improved slightly but remains cautious and below historical norms. The Conference Board’s Index of Consumer Confidence held at 47.8 in September 2025, essentially unchanged from August and still under its long-term average. The Bank of Canada’s survey echoed this caution, showing weaker spending intentions and rising concerns about household finances, job security, and trade uncertainty. While inflation has eased somewhat, high borrowing costs and slower growth continue to weigh on overall confidence. (Source: Conference Board of Canada)

Consumer spending is also showing signs of moderation. Retail sales likely fell 0.7% in September after rising 1.0% in August, following a brief rebound earlier in the summer. Card-spending growth slowed sharply to about 1.5% year over year in Q2 from over 5% in Q1, suggesting that households are tightening budgets. Forecasts now call for consumer spending to grow roughly 2% in 2025, easing to under 1% in 2026, as higher rates and economic uncertainty temper discretionary outlays. (Source: TD Economics & Fitch Ratings)

Earnings – U.S. and Canadian Markets

More than halfway through the third-quarter earnings season, the S&P 500 is delivering a mixed but generally positive performance. About 64 % of companies have reported results, with 83 % beating EPS estimates—well above the 5-year average of 78 % and the 10-year average of 75 %. However, the size of these earnings beats is smaller than usual, with results coming in roughly 5.3 % above estimates, compared with a 5-year average of 8.4 %. Despite the narrower margin, the index is still on track for its fourth straight quarter of double-digit earnings growth, supported by solid revenue gains across most sectors.

Sector trends are driving the variation beneath the surface. Information Technology, Consumer Discretionary, and Health Care companies have provided the strongest upside surprises, helping lift the overall earnings growth rate, while Communication Services and Industrials have been modest drags. Financials have also contributed positively since the quarter’s start, reinforcing the picture of an economy that remains resilient but uneven. Overall, the data point to a constructively balanced earnings environment—profits are growing solidly, but at a more sustainable pace, reflecting a gradual normalization after several years of outsized corporate performance. (Source: Factset)

Although detailed TSX-specific data are less current in public summaries, Canada’s Q3 2025 earnings season has been broadly constructive, led by strong results from the banking and energy sectors. Major banks reported roughly 5 % quarter-over-quarter revenue growth and 12 % year-over-year gains, driven by resilient net interest income and lower provisions for credit losses. TD and CIBC both beat consensus estimates as loan growth and fee income held firm, though management guidance reflected caution about slower economic momentum.

Canada’s energy sector delivered a strong third quarter in 2025, driven by record production volumes and operational efficiency despite weaker crude prices. The sector’s resilience stems largely from cost control, integration, and volume growth, not price strength, as firms navigate wide WTI–WCS spreads and trade uncertainty. Strategic consolidation, such as Cenovus’s planned C$7.9 billion acquisition of MEG Energy, underscores a focus on scale and efficiency. Overall, the energy sector remains a pillar of Canadian earnings, balancing disciplined execution with cautious outlooks amid softer commodity markets.

Summary

As we move into the final stretch of 2025, markets appear to be settling into a more balanced rhythm, one defined less by fear of policy missteps and more by an acceptance of slower, steadier progress. While volatility remains part of the landscape, inflation is trending lower, earnings remain broadly resilient, and the worst-case scenarios around trade and fiscal tightening have so far been avoided. This environment argues for patience and selectivity rather than retreat. Investors emphasizing quality, liquidity, and disciplined risk management are well positioned to benefit as valuations and fundamentals begin to realign more sustainably.

Caution, however, should not be mistaken for pessimism. Opportunities continue to emerge beneath the surface, particularly across sectors benefiting from structural trends in innovation, infrastructure renewal, and energy transition. In both the U.S. and Canada, corporate balance sheets remain strong, dividend growth is stable, and capital investment, though slower, is becoming more targeted and efficient. For long-term investors, this phase of recalibration offers a constructive backdrop to accumulate quality assets at more reasonable valuations, while remaining mindful of macro risks that could test sentiment along the way.

Ultimately, 2025 may be remembered less for exuberant rallies and more for the quiet groundwork being laid for the next expansionary cycle. Fiscal restraint, gradual monetary easing, and resilient earnings together point toward a soft-landing scenario that, while imperfect, is far preferable to the alternatives feared just a year ago. As policymakers and businesses alike adapt to this new equilibrium, maintaining a disciplined yet optimistic outlook will be key, anchored in diversification, prudence, and confidence in the long-term strength of North American markets.

We thank you for your continued trust and we welcome you to reach out to us with any questions you may have.

This information has been prepared by Kian Ghanei and Terry Fay who are Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.