If January was about setting expectations, February was about meeting them. Markets entered 2026 with a cautiously constructive view of the world, inflation trending in the right direction, rate cuts still within reach, and corporate earnings expected to hold their ground. For the most part, that is exactly what happened.

Across the United States and Canada, fourth-quarter results came in better than many had feared. Profit growth held up. Margins stabilized. Credit conditions stayed manageable. The soft-landing narrative that so many had debated through 2025 not only survived the month, it gained credibility.

That said, February also served as a reminder that encouraging data is not the same as a clear path forward. Market performance remains concentrated in a handful of sectors. Valuations in certain areas have moved well above historical norms. Geopolitical uncertainties continue to simmer in the background making it difficult to price assets correctly in the face of a ever changing market sentiment.

U.S. Earnings: Still Expanding

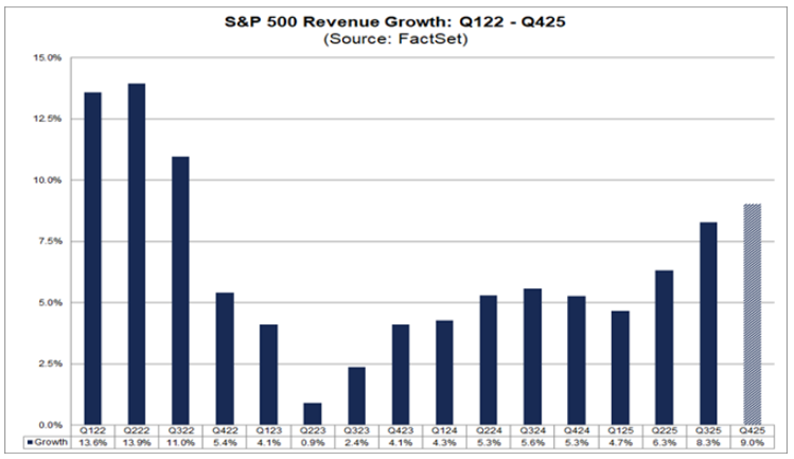

With the majority of S&P 500 companies now having reported fourth-quarter results, blended earnings growth came in around the mid-to-high single-digit range year-over-year. On the surface that may not sound like much, but given the backdrop of persistently higher borrowing costs and a gradually slowing economy, it is a genuinely solid result.

Revenue growth held up across a broad range of sectors, and perhaps more importantly, profit margins stabilized after taking a beating during the inflation surge of 2022 and 2023. Companies have been quietly doing the work of adapting, cutting costs where they needed to, improving efficiency, and holding onto pricing power in the areas that matter most.

Forward guidance from management teams was generally measured and steady. Few companies are calling for a big acceleration in growth, but most are not bracing for a downturn either. The tone across earnings calls was cautious in places, but not defensive.

Valuations have moved to reflect that resilience. The forward price-to-earnings ratio for the S&P 500 sits near 20 to 21 times earnings, which is above long-term historical averages and warrants some attention. That said, this is not a situation where valuations are being supported by hope alone. Earnings are actually growing into those multiples, which is a meaningful distinction when trying to assess whether today’s prices are genuinely supported or simply optimistic. (Source: FactSet & Bloomberg Intelligence)

Artificial Intelligence: The Dominant Force

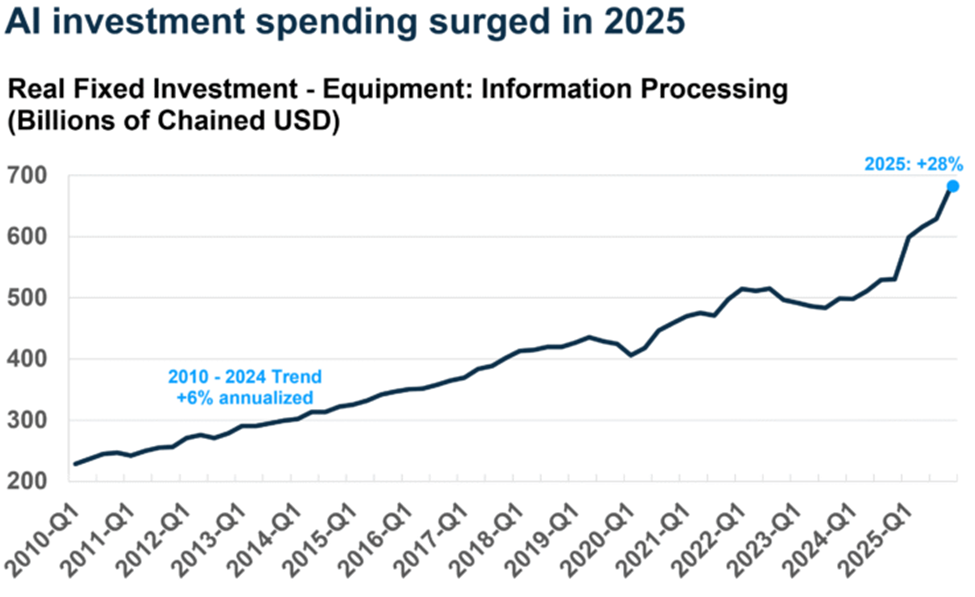

You cannot talk about this earnings season without talking about artificial intelligence. It is the dominant force shaping where capital flows, which companies lead, and what investors are willing to pay.

Technology companies are still pouring money into data centers, semiconductors, and software infrastructure. But what has shifted over the past few quarters is that enterprises are no longer just experimenting with AI, they are deploying it. That transition from pilot projects to actual implementation is starting to show up in financial results in meaningful ways. AI is no longer a line item in a future business plan. It is a revenue line today.

NVIDIA Corporation once again captured the market’s attention with results that were hard to dismiss. Data center revenue growth remained strong, margins expanded, and management signaled that order activity heading into 2026 shows no signs of letting up. Investors largely read this not as peak enthusiasm but as confirmation that the underlying investment cycle still has room to run. (Source: Goldman Sachs Strategy Research, Reuters)

The U.S. Economy: Slowing, Not Stalling

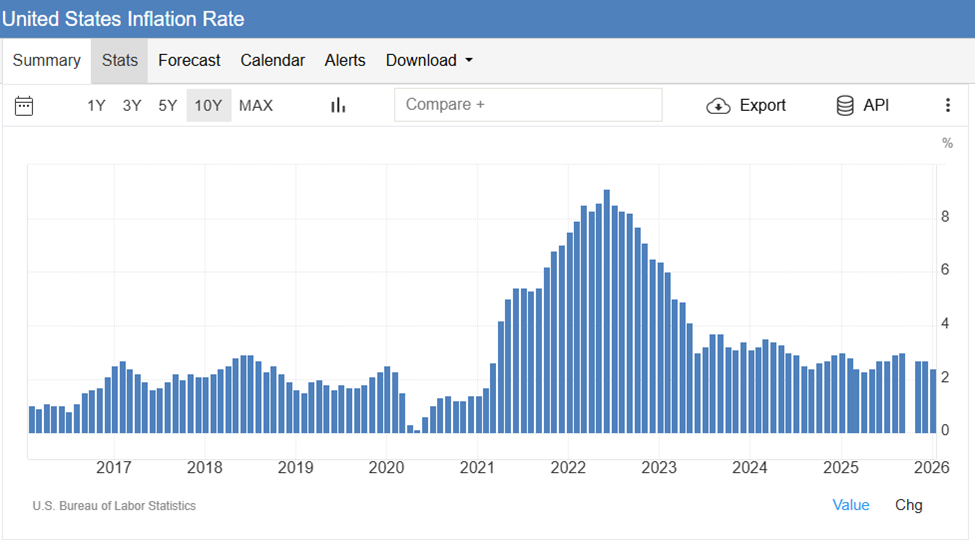

The broader economic picture in the United States continues to hold together better than many expected a year ago. GDP growth has come down from its post-pandemic pace, but it remains positive. Consumer spending has eased at the margin without falling off a cliff. The labour market is no longer tightening the way it was through 2023 and 2024, but unemployment remains low by any reasonable historical measure.

Put simply, the economy looks like it is normalizing rather than deteriorating, and that is almost exactly what the Federal Reserve has been trying to engineer. The goal all along was to bring inflation back toward target without forcing a hard stop in economic activity, and so far that outcome appears to be taking shape.

Inflation continues to trend in the right direction, with the latest reading sitting at 2.4%. Core measures remain a bit sticky, particularly in services, but the overall trajectory is constructive. (Source: US Bureau of Economic Analysis & Trading Economics)

Canada: Steady

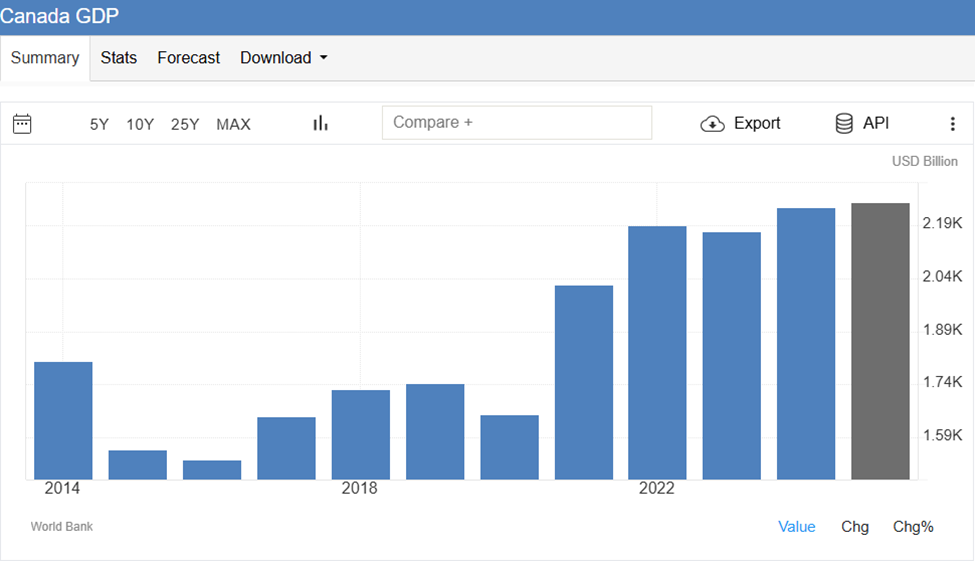

Canadian earnings season carried a more measured tone, but measured does not mean concerning. The country’s major banks, Royal Bank of Canada, TD, Bank of Nova Scotia, Bank of Montreal, and CIBC, reported modest loan growth and provisions for credit losses that, while still running above pre-pandemic levels, have stabilized quarter over quarter. Capital ratios remain solid. Dividends remain intact. Net interest margins have largely found their footing. These are not exciting results, but they are the kind of steady, reliable results that income investors count on, and they delivered.

The broader Canadian economic backdrop reflects that same sense of steadiness. GDP growth has been modest but intact. Inflation has come a long way from its peak. The Bank of Canada has been deliberate about signaling caution before making further policy moves, a posture that makes sense given how much has changed over the past two years and how much uncertainty still surrounds the path ahead. (Source: Trading Economics, TD Research, World Bank)

Trade & CUSMA: A Pivotal Few Months Ahead

On February 20th, the U.S. Supreme Court struck down President Trump’s 35% IEEPA tariffs in a 6 to 3 ruling, a genuinely meaningful development for Canada. Those duties had been sitting over trade confidence like a cloud since they were first introduced, and their removal provides some welcome relief. The same day, however, the administration responded by introducing a new 10% global tariff under Section 122 of the 1974 Trade Act. The important caveat is that CUSMA-compliant goods remain exempt, which means the large majority of Canadian exports into the United States continue to move without additional duties. Sectoral tariffs on steel, aluminum, lumber, and autos were not affected by the Supreme Court ruling and remain in place.

The larger story, though, is the CUSMA review that is now moving toward a real deadline. All three countries need to signal their intentions by July 1, 2026, and formal Canada-U.S. negotiations have not yet formally begun, though meetings are expected imminently. U.S. Trade Representative Jamieson Greer has been straightforward in saying that Canada will need to accept some level of higher tariffs under any new framework, and that Washington is pushing for greater domestic manufacturing content, particularly in the auto sector. Canada comes to this table with real leverage of its own, including critical minerals, energy supply relationships, and the credible ability to diversify trade toward other partners. How this plays out over the next few months will have meaningful consequences for Canadian investment activity, employment, the currency, and business confidence more broadly. (Source: CBC News, BNN Bloomberg)

Risks Worth Respecting

Not everything about the current environment calls for optimism. Valuations in certain sectors have moved well above comfortable levels. Market leadership remains narrower than most investors would like. Geopolitical tensions have not gone away. Trade policy, regional conflicts, and political cycles all introduce uncertainties that are genuinely difficult to measure but tend to become very visible very quickly when market sentiment turns.

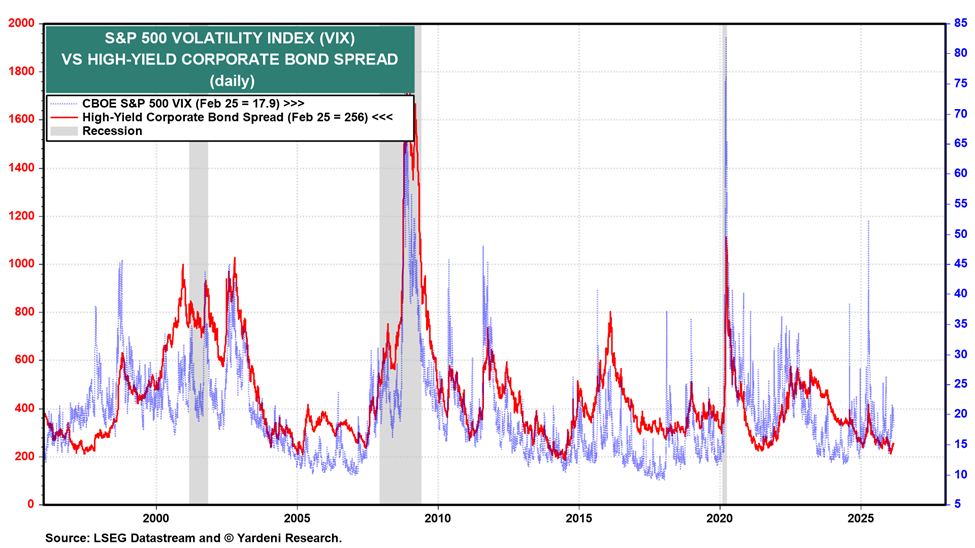

The Volatility Index (VIX)

One of the more useful ways we track the overall health of market sentiment is by watching the relationship between the S&P 500 Volatility Index, the VIX, and the high-yield corporate bond spread. The VIX captures what equity markets expect in terms of near-term volatility.

The high-yield spread tells you what bond investors are demanding to hold riskier corporate debt instead of government bonds. When both are low and calm, as they have largely been over recent months, it reflects an environment where credit is flowing, risk appetite is healthy, and investors feel comfortable. That backdrop has been genuinely supportive of equity performance.

We watch this relationship closely not because it tells us what is about to happen, but because it gives us a real-time read on how much risk the market is quietly absorbing and how durable that calm actually is. (Source: LSEG Datastream & Yardeni Research)

Producer Prices

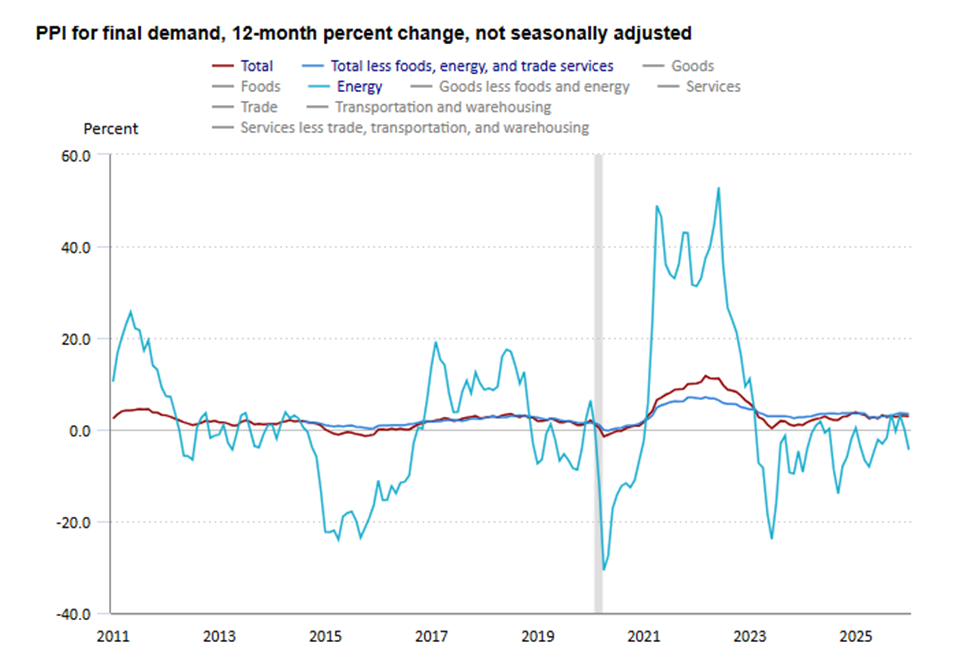

January’s Producer Price Index came in at 0.5% for the month, above the consensus estimate of 0.3%, and the headline number was enough to send the Dow down over 500 points on the day of the release. That kind of reaction is understandable when the number first lands, but a closer look at what actually drove it tells a more reassuring story. Goods prices declined 0.3% in January, led by a 5.5% drop in gasoline and a 1.5% decline in food prices. The entire upside surprise was concentrated in one corner of the services category, specifically profit margins for professional and commercial equipment wholesalers, which jumped 14.4% and on their own accounted for more than 20% of the overall services increase. That is a measure of what businesses decided to charge, not evidence of tariff costs working their way through the supply chain. There is no clear sign at this point that broad-based tariff-induced inflation is showing up at the producer level. That could change as trade negotiations develop over the coming months, and it is something we will continue to watch closely. But for now, January’s PPI is a headline that deserves more context than it typically received. (Source: Bureau of Labor Statistics)

Summary: Staying Grounded

What stands out most about February is not excitement or exuberance. It is resilience. Corporate earnings are growing into their valuations. Artificial intelligence continues to reshape how capital is allocated and where growth is being built. Economic growth is slowing, but it is not stalling. Taken together, that is a genuinely constructive backdrop for investors who remain thoughtful about how they are positioned.

At the same time, we think disciplined portfolio construction matters more, not less, in an environment like this one. This is precisely where our ADAPT Investment Process provides a meaningful framework for navigating what comes next. ADAPT is built around the recognition that markets are always changing, and that the portfolios most likely to protect and grow wealth over time are those that remain anchored to fundamentals while staying flexible enough to respond to new information.

The signals we are watching today, from earnings trends and AI-driven investment cycles to central bank policy and the evolving CUSMA negotiations, all feed directly into how we think about positioning and risk. History has been consistent on one point: the moments when investor confidence runs highest are often the moments when overlooked risks are quietly building. That is not an argument for stepping away from markets. It is an argument for staying engaged within them thoughtfully, with diversified exposure, measured participation in structural growth themes, and the discipline to adapt when conditions change.

We thank you for your continued trust and welcome you to reach out to our team with any questions you may have.

This information has been prepared by Kian Ghanei, a Senior Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.