Turning Points

May was anything but quiet. Investors navigated a complex mix of geopolitical developments, strong corporate earnings, persistent inflation concerns, and markets that continued to advance despite widespread uncertainty. Yet when we step back from the daily headlines, the broader picture is one of resilience. Economic growth has moderated, but corporate profits remain healthy, consumers continue to spend, and financial markets have demonstrated a remarkable ability to adapt to changing conditions.

The conflict in the Middle East remained one of the dominant market themes throughout the spring. As tensions escalated in March, we took the prudent step of reducing our equity exposure in response to a highly uncertain and unpredictable environment. By April, however, hostilities had eased considerably, helping restore investor confidence and allowing markets to refocus on economic fundamentals, corporate earnings, and long-term growth opportunities. That shift in sentiment has been an important driver of market performance in recent months.

As Portfolio Managers, periods like these serve as a reminder that markets are rarely comfortable. Uncertainty is often the price investors pay for long term returns. While risks remain, the ability of markets to absorb challenges and continue moving forward reinforces the importance of maintaining a disciplined investment approach focused on long term fundamentals rather than short term headlines.

The Middle East: A Fragile but Encouraging Path Forward

May began with renewed tensions in the Middle East as military strikes and increasingly aggressive rhetoric raised concerns that the diplomatic progress achieved earlier in the year could unravel. Financial markets responded accordingly, with oil prices moving higher and equities experiencing increased volatility as investors assessed the potential economic consequences of a broader conflict.

The tone improved significantly as the month progressed. By late May, negotiations between the United States and Iran had resulted in an agreement to extend the existing ceasefire and begin formal discussions regarding Iran’s nuclear program. Importantly, the agreement included measures aimed at preserving commercial shipping through the Strait of Hormuz, a critical artery for global energy markets. The prospect of greater stability helped push oil prices lower from their mid month highs, eased pressure on bond yields, and supported equity markets, including Canada’s banking sector and the broader TSX Index.

While uncertainty has not disappeared and further diplomatic progress will be required, the direction of travel is encouraging. A lasting reduction in tensions would support global supply chains, reduce pressure on energy prices, and improve the inflation outlook. For investors, those developments would create a more constructive backdrop for both economic growth and financial markets in the months ahead. (Sources: CNBC; Polymarket)

AI Infrastructure: The Build-Out Accelerates

Semiconductors: Powering the Next Phase of AI Growth

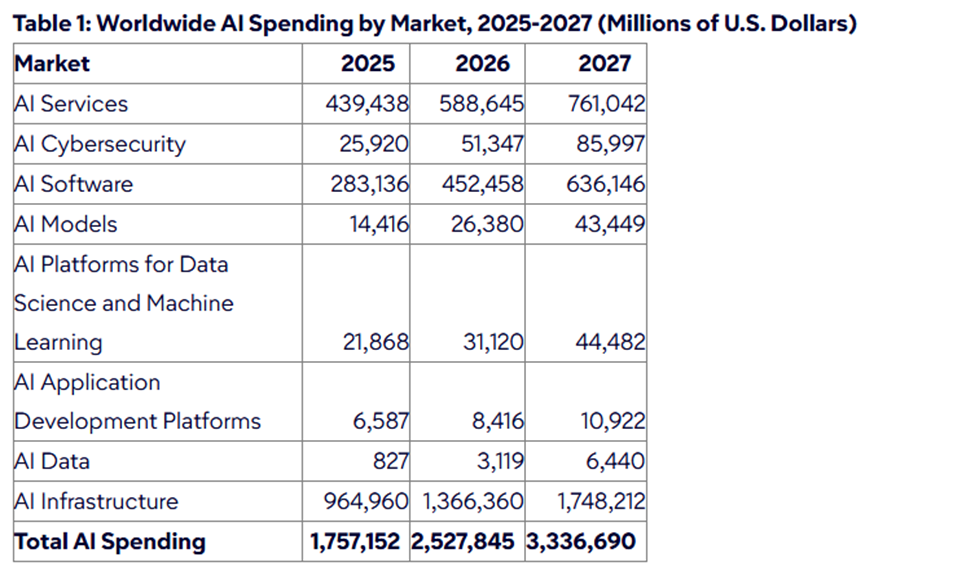

The semiconductor industry is experiencing unprecedented growth as artificial intelligence continues to reshape the global economy. Industry forecasts suggest global chip sales could exceed $1.3 trillion in 2026, driven largely by demand for AI related computing. Major technology companies including Google, Amazon, Meta, and Microsoft are collectively investing hundreds of billions of dollars into AI infrastructure, fueling demand for advanced processors, memory chips, networking equipment, and digital storage systems. What was once viewed as a technology trend has evolved into one of the largest infrastructure investment cycles in modern history. On an accelerated basis, Gartner projects worldwide spending on AI will exceed $2T by the end of 2026. (Source: Gartner.com)

While NVIDIA remains the dominant supplier of AI chips, the benefits are spreading across the broader semiconductor ecosystem. Companies such as AMD, Intel, Broadcom, Samsung, Micron, SK Hynix, and Taiwan Semiconductor are all seeing increased demand as organizations expand their computing capacity. A notable shift is also occurring in the types of chips required. While graphics processing units remain critical for training AI models, growing adoption of agentic AI applications is increasing demand for central processing units that can manage databases, automate workflows, and support enterprise computing tasks. This broadening demand profile suggests the AI opportunity is becoming more diversified and sustainable.

Importantly, the AI buildout extends far beyond semiconductors alone. The rapid growth of artificial intelligence requires enormous investments in data centers, cloud storage, fiber optic networks, electricity generation, power transmission systems, and critical minerals such as copper, uranium, and rare earth elements. These technologies form the physical backbone of the digital economy. For investors, this means the beneficiaries of AI extend well beyond technology companies to include utilities, infrastructure providers, industrial firms, energy producers, and resource companies. As AI adoption continues to accelerate, the buildout of this supporting infrastructure is likely to remain one of the most important long term investment themes of the coming decade.(Sources: CNBC; TechJournal; Gartner, FactSet)

Inflation: The Energy Wildcard

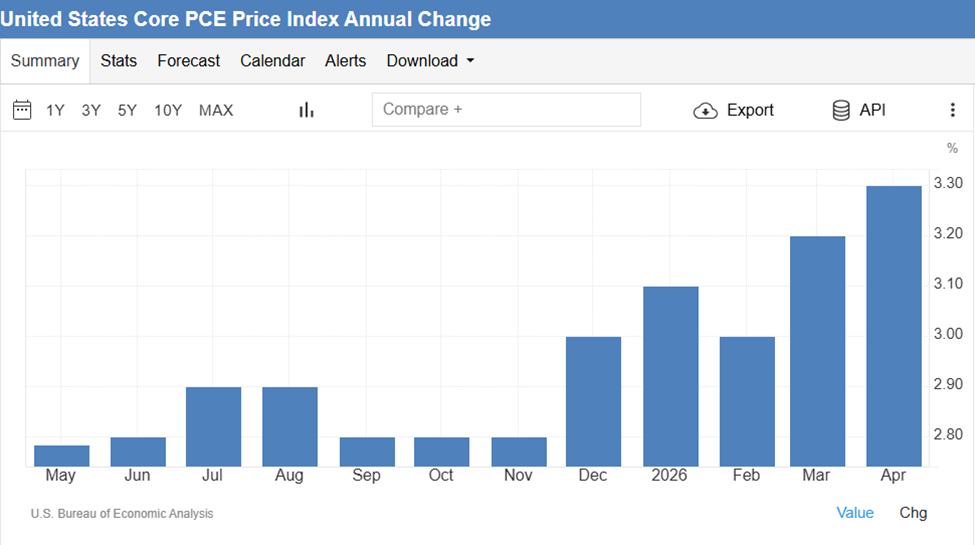

Inflation remains one of the most closely watched variables in the global economy as we move through 2026, and recent data continues to present a mixed picture. While inflation remains above central bank targets, much of the recent pressure has been tied to energy markets rather than broad-based economic overheating. This distinction is important because it suggests that some of the recent inflationary pressures may prove temporary rather than structural.

The latest inflation data showed consumer prices rising at a faster pace than expected, driven primarily by higher energy costs. Gasoline prices increased sharply following supply disruptions and geopolitical tensions in the Middle East, reminding investors how sensitive inflation can be to global energy markets. Core inflation, which excludes the more volatile food and energy components, has remained considerably more contained. While still above central bank targets, core price pressures continue to move in a more encouraging direction and suggest underlying inflation trends are gradually moderating. (Source: Trading Economics)

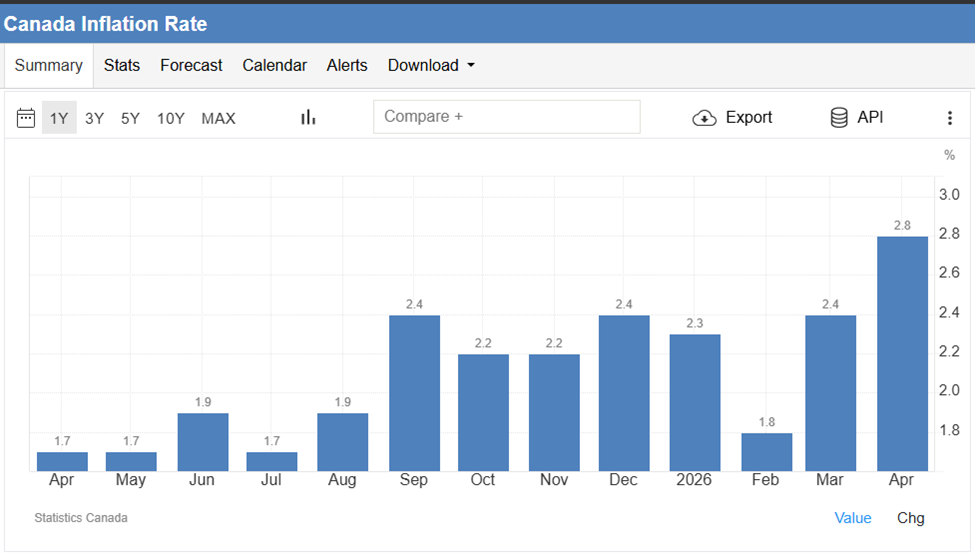

In Canada, The headline inflation rate in Canada rose to 2.8% in April of 2026 from 2.4% in the previous month, the highest in two years, albeit firmly under the market consensus of 3.1%.The Bank of Canada’s policy rate currently sits at a level many economists consider broadly neutral, allowing policymakers flexibility as they assess evolving economic conditions. South of the border, the U.S. Federal Reserve has maintained a patient approach, balancing persistent inflation pressures against signs of moderating economic growth. While interest rate cuts may not be imminent, neither do policymakers appear eager to tighten further unless inflation proves more persistent than expected.

Looking ahead, energy prices remain the key variable to watch. Should geopolitical tensions continue to ease, and global oil supplies normalize, energy costs could move lower in the months ahead, helping reduce headline inflation readings. Such an outcome would provide additional support for consumers, businesses, and financial markets while increasing the likelihood that central banks can eventually shift their focus from fighting inflation toward supporting economic growth.Sources: U.S. Bureau of Labor Statistics (CPI, April 2026); CNBC; Bank of Canada Policy Statements)

Corporate Earnings: Strong Results Continue

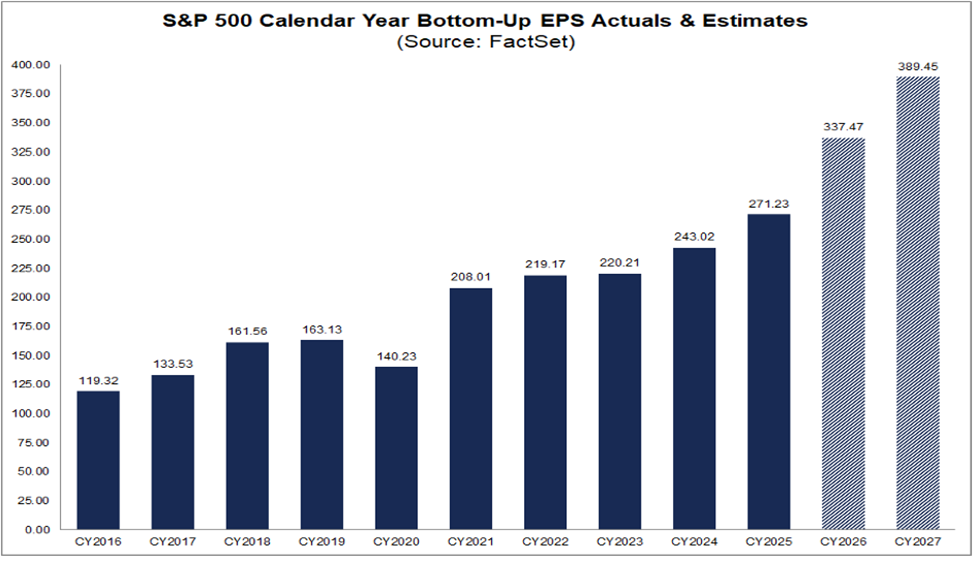

Despite ongoing geopolitical uncertainty, elevated energy prices, and a mixed economic backdrop, corporate earnings have remained a significant source of strength for equity markets. First quarter results demonstrated that many businesses continue to adapt well to changing economic conditions, with profitability and revenue growth exceeding expectations across a broad range of industries.

With the vast majority of S&P 500 companies having reported first quarter results, earnings season delivered some of the strongest results seen in recent years. Approximately 84% of companies exceeded analyst earnings expectations, well above historical averages. Overall earnings growth came in substantially ahead of forecasts, highlighting the resilience of corporate America despite concerns surrounding inflation, interest rates, and global economic growth. Analysts currently expect S&P 500 earnings to grow by roughly 21% in 2026, with profit margins remaining healthy and forecasts calling for continued expansion through the remainder of the year. While equity valuations remain above long-term averages, an increasing portion of those valuations is being supported by genuine earnings growth rather than investor optimism alone.

In Canada, the story has been similarly encouraging. Major banks including Royal Bank, TD, and BMO reported solid results supported by strong capital positions and resilient lending activity. Taken together, the earnings season reinforced a theme that has become increasingly evident throughout 2026: while economic growth may be moderating, corporate fundamentals remain considerably stronger than many investors anticipated, providing an important foundation for financial markets moving forward. (Source: Trading Economics)

Canada’s Sovereign Fund

The Canada Strong Fund is Canada’s first national sovereign wealth fund, announced by Prime Minister Carney on April 27 and seeded with an initial $25 billion from the federal government. It will operate as an independent Crown corporation, investing alongside the private sector in what the government calls “nation building” projects, spanning nuclear energy, LNG, critical minerals, agriculture, and major transportation infrastructure. A genuinely novel feature is a planned retail investment product that will allow ordinary Canadians to buy into the Fund directly and share in its financial returns, much like a government bond or mutual fund. The Major Projects Office has already identified 15 projects and six transformative strategies representing more than $126 billion in total investment potential.

The Fund’s purpose is straightforward: reduce Canada’s economic dependence on U.S. market access, attract private capital into projects that are too large or complex for the private sector to finance alone, and build long term productive capacity at home. By investing alongside private and institutional capital, the Fund aims to encourage financing for projects that might otherwise struggle to move forward because of their scale, risk profile, or lengthy development timelines. The Fund is not yet fully operational, as enabling legislation and parliamentary authorization are still required. However, the government has established a transition office and expects the Fund to be functional within months.

The challenges are significant and warrant close attention. Unlike Norway’s sovereign wealth fund, which was built using oil revenue surpluses, Canada is borrowing to capitalize this vehicle while facing a $66.9 billion deficit and debt servicing costs projected to reach $81 billion by 2030 31. Critics also note that Canada already has the Canada Infrastructure Bank, the Business Development Bank, and numerous other public financing vehicles. Between 2015 and 2024, more than $1 trillion in net investment left Canada despite billions already deployed through these institutions, suggesting that the primary obstacles may be regulatory delays and slow approval processes rather than a lack of public capital. Ultimately, project selection, governance, and the extent of regulatory reform accompanying the Fund will determine whether it becomes a transformative institution or simply another layer within Canada’s existing public financing framework. (Source: Canada.ca and CBC)

Staying the Course

As we move into the second half of 2026, the investment landscape remains defined by both opportunity and uncertainty. Geopolitical tensions, inflation concerns, and evolving trade relationships continue to create headlines and periods of market volatility. Yet beneath that noise, several important fundamentals remain supportive. Corporate earnings have been stronger than expected, the AI infrastructure buildout continues to drive substantial investment across multiple industries, inflation pressures appear increasingly concentrated in energy markets, and Canada’s economy continues to demonstrate resilience despite a slowing growth environment.

Perhaps the most important takeaway from May is that markets continue to reward patience and discipline. While we remain attentive to risks and prepared to adjust portfolios when conditions warrant, we continue to see reasons for cautious optimism. Innovation, infrastructure investment, healthy corporate balance sheets, and improving geopolitical conditions all provide a foundation for continued economic and market progress. As always, our ADAPT Investment Strategy will focus on preserving capital, identifying attractive opportunities, and positioning portfolios to participate in long term growth while managing risk appropriately.

We thank you for your continued trust and welcome you to reach out to our team with any questions you may have.

This information has been prepared by Kian Ghanei, a Senior Portfolio Managers for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The [Investment Advisor/Portfolio Manager] can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.